Chain link (source: Pixabay)

Chain link (source: Pixabay) Blockchain is a solution for business networks. It makes sense to deploy a blockchain-based solution only where there is a network of collaborating participants who are issuing transactions around a set of common assets in the network. In this article, we’ll identify the initial crucial steps to identifying scenarios for a successful blockchain-based solution, and the first steps toward transforming your business model.

Our first observation of when blockchain is the right solution is that there must be a business network of multiple participants. Our second would be that they require a shared view of assets and their associated transactions.

We then use the following four key blockchain features to further define the benefits of a blockchain-based solution:

Consensus

The process of agreeing on new transactions and distributing them to participants in the network.

Provenance

A complete history of all transactions related to the assets recorded on the blockchain.

Immutability

Once a transaction has been stored on the blockchain, it cannot be edited, deleted, or have transactions inserted before it.

Finality

Once a transaction is committed to the blockchain, it is considered “final” and can no longer be “rolled back” or undone.

There are several other blockchain benefits that underpin these four key benefits, and are worth keeping in mind as you review any potential scenarios:

Identity

All participants in a permissioned blockchain network have an identity in the form of a digital certificate—the same technology that underpins the security and trust when we use a web browser to access our online bank.

Security

Every transaction in the permissioned network is cryptographically signed, which provides authenticity of which participant sent it, nonrepudiation (meaning they can’t deny sending it), and integrity (meaning it hasn’t been changed since it was sent).

Contracts

Smart contracts hold the business logic for transactions and are executed across the network by the participants endorsing a transaction.

These benefits help engender trust between the participants in busi‐ ness networks, and we can use them as a litmus test when checking to see if blockchain is a good technology fit. We should note that while it’s not necessary for a scenario to require every benefit just listed, the more that are required, the more the case is strengthened for using blockchain.

We should always be wary of thinking that blockchain is a panacea for all solutions. There are many reasons why blockchain wouldn’t be a good fit. For example:

- Blockchain is not suitable if there’s only a single participant in the business network.

- Although we talk about transactions and world state databases in blockchain, it shouldn’t be thought of as a replacement for traditional database or transaction servers.

- Blockchain by design is a distributed peer-to-peer network, and is heavily based on cryptography. With this comes a number of nonfunctional requirement considerations. For example, performance and latency won’t match a traditional database or transaction server, but scalability, redundancy, and high availability are built in.

Assets, participants, and transactions

When thinking about a potential blockchain solution and the benefits it brings to the network of participants, it is useful to view it in relation to the following concepts:

- Assets

- Participants

- Transactions

We have already introduced some examples of these. They are core concepts in a blockchain network that benefit from the four primary trust benefits introduced in the previous section.

Assets

Either purely digital, or backed by a physical object, an asset represents something that is recorded on the blockchain. The asset may be shared across the whole network, or can be kept private depending on the requirements. A smart contract defines the asset.

Participants

Participants occupy different levels in a blockchain network. There are those participants who run parts of the network and endorse transactions. Other members may consume services of the network but may rely on and trust other participants to run the network and endorse transactions. Then there are the end users who are interacting with the blockchain network through a user interface. The end user may not even be aware that a blockchain underpins the system.

Transactions

The transactions are coded inside the smart contracts alongside the assets to which the transactions belong. Think of the transactions as the interaction points between the assets and the participants; a participant can create, delete, and update a given asset, assuming they are authorized to do so. It is these transactions that are stored immutably on the blockchain, which also provides the provenance of any changes to the asset over time.

The blockchain fit

First and foremost is to check there is a business network in place. Identify how many suppliers and partners are involved in both the internal and external network. If there is a good business network in place, consider the rest of the blockchain features.

As some of the disputes are related to differences between what was ordered and subsequently received, this can often be the result of different participants in a business network (partners, suppliers, and delivery companies) tracking goods in separate siloed systems.

Therefore, a shared ledger with consensus and finality provided by blockchain across the business network will help to reduce the overall number of disputes as it will give all participants the same information on the assets being tracked.

Furthermore, if changes to the data being tracked either intentionally or unintentionally are part of the root cause of these disputes, then the provenance and immutability features of blockchain could also help.

Last, consider the amount of time taken to resolve these issues. If there are multiple systems (including third-party systems) that someone needs to check in order to resolve any transactions in dispute, having a single shared ledger that is maintained through consensus will help reduce the time taken to resolve them.

Some further observations about how a blockchain-based solution can benefit this business network:

- Each participant in the business network has an identity and is permissioned in the network. This could help with your processes related to know your customer (KYC) and anti-money laundering (AML).

- Smart contracts could be designed to resolve some of the disputes automatically by maintaining consistency across the business network and therefore further reducing the number of disputes.

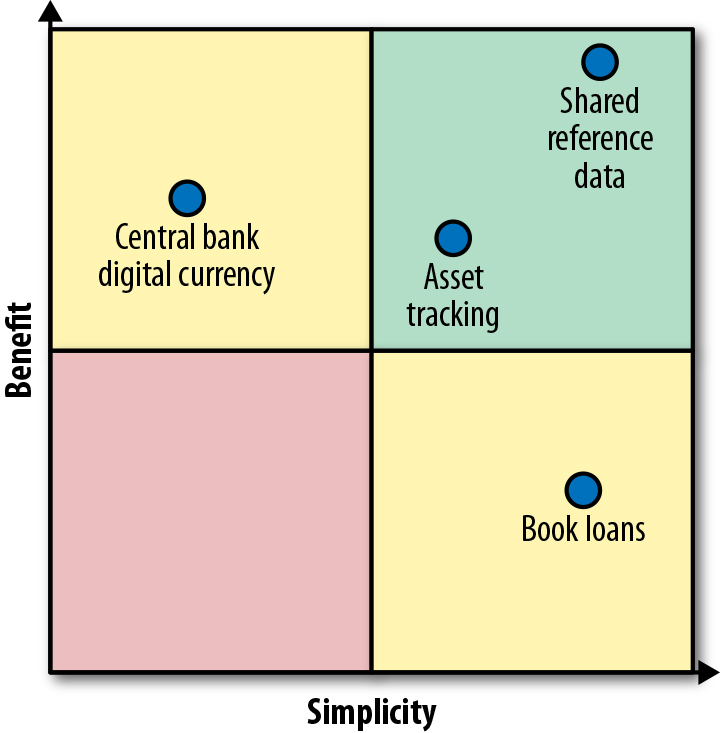

Choosing a first scenario

You may be considering multiple scenarios where blockchain provides a good solution fit. In this case, you will need to compare each to determine which is the best scenario to work on first.

We recommend a simple approach for comparing each scenario using a quadrant chart, where each is placed on the chart based on its relative benefit and simplicity.

In Figure 1, the x-axis is the simplicity of the scenario (simpler to the right) and the y-axis represents the benefit (more beneficial to the top). Place each scenario on the quadrant chart, considering its expected benefit and simplicity as a blockchain solution. This is best done as a group exercise with appropriate stakeholders who can provide the necessary insight to where each scenario falls in the chart based on level of simplicity and potential benefits.

Once all scenarios have been plotted on the chart, it becomes obvious which are the first scenarios to concentrate on—those that will provide the most benefits and are the simplest.

Transforming the business network

Once your first blockchain scenario has been identified, you will want to move to the next phase: building the minimal viable product (MVP). An MVP represents the minimum product that can be built to accomplish a goal of the blockchain scenario. Starting an MVP with blockchain shouldn’t be dissimilar to any other technology, and good software engineering practices, such as using Agile principles, will always be applicable. Following are some observations that will help as you start to transform your business with a new blockchain-based solution:

- Blockchain is a team sport. There will be multiple stakeholders from different organizations in the business network. Some of these organizations may not have traditionally worked directly with one another. Therefore, a clear understanding of the requirements and issues across all participants, and clear lines of communication and agreement, are critical to the success of the project.

- Use design thinking techniques that focus on the goals for the user to agree on the scope of the MVP.

- Use agile software engineering best practices, such as continuous integration and stakeholder feedback, to iterate throughout the development of the MVP. Keep stakeholders informed and act on feedback.

- Start with a small network and grow. There will be some challenges ahead, as this may be a paradigm shift for the business network.

- If replacing an existing system, consider running the blockchain-based solution as a shadow chain to mitigate risk. By this we mean, during the pilot phase, run the new platform alongside the legacy system. Ideally, you would pass real production data to the new blockchain-based system to test and validate it, while continuing to rely on the legacy system for this phase of the project. Only after thorough testing has been completed and the new system has been proven should you switch from the legacy system to the new.

- Although blockchain is likely to be a core foundational part of the solution, it probably won’t be the majority. The blockchain network will still integrate with other external systems, providing additional functions such as off-chain data storage, identity access management, Application Programming Interface (API) management and presentation layers, and so on.

Read the full free ebook here.

This post is a collaboration between O’Reilly and IBM. See our statement of editorial independence.