CHAPTER 11Some Suggestions to Improve the Current Situation

Corruption, embezzlement, fraud, these are all characteristics which exist everywhere. It is regrettably the way human nature functions, whether we like it or not. What successful economies do is keep it to a minimum. No one has ever eliminated any of that stuff.

—Alan Greenspan (former president of the US Federal Reserve, 2007)

As we have been seeing throughout the book, accounting fraud is lethal for companies and those who have trust in them. It damages trust in the economic system of a country, as well as its companies and institutions. It also affects negatively the accounting and auditing profession. Therefore, it is necessary to fight fraud with all possible weapons.

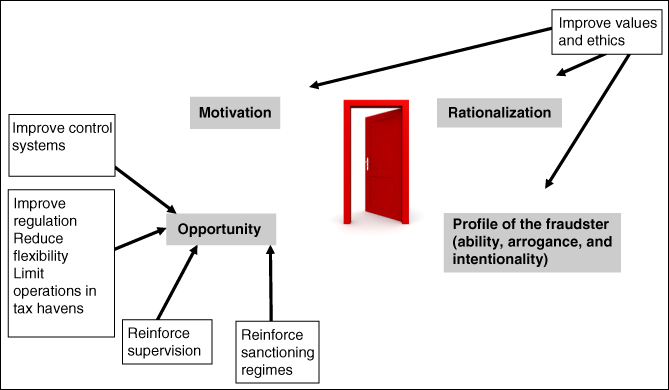

In this chapter we propose measures that could reduce deceits and improve the reliability of the companies' financial information. As shown in Figure 11.1, and remembering the concept of the door to fraud, these measures are proposed to act against the four big factors that explain the occurrence of frauds.

FIGURE 11.1 The door to fraud and several measures to reduce frauds

11.1 REINFORCE VALUES AND INSTITUTE ETHICAL CODES

Fraud and deceit are inherent to the human condition. It isn't realistic to imagine a world without fraud. However, as the populations' values improve, frauds will reduce. Therefore, a key element in the fight against accounting ...

Get Detecting Accounting Fraud Before It's Too Late now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.