CHAPTER 7

INVENTORY AND ACCOUNTS PAYABLE

Acquiring Inventory on the Cuff

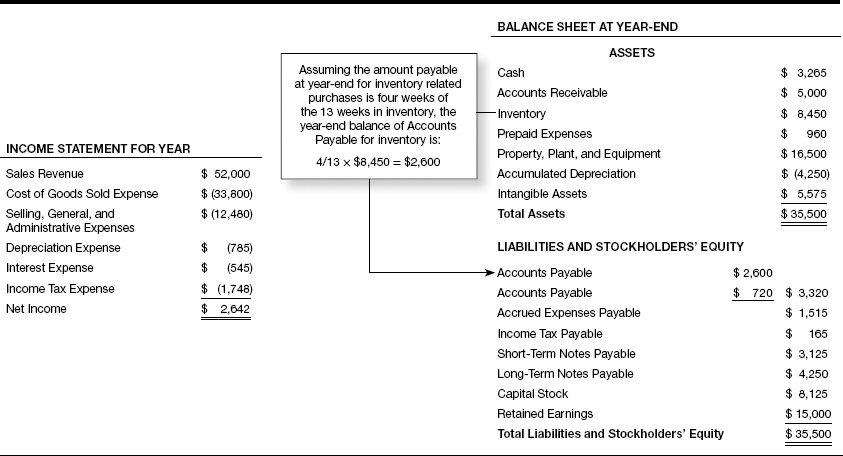

Please refer to Exhibit 7.1 at the start of the chapter. This chapter focuses on the connection between the inventory asset account in the balance sheet and the accounts payable liability in the balance sheet. Virtually every business reports accounts payable in its balance sheet, which is a short-term, noninterest-bearing liability arising from buying services, supplies, materials, and products on credit.

EXHIBIT 7.1—INVENTORY AND ACCOUNTS PAYABLE

Dollar Amounts in Thousands

One main source of accounts payable is from making inventory purchases on credit. A second source of accounts payable is from expenses that are not paid immediately. Therefore, at this point we divide the total balance of the company’s accounts payable liability into two parts, one for each source (refer to Exhibit 7.1 again).

The previous two chapters connect an income statement account with a balance sheet account. In this chapter we look at a connection between two balance sheet accounts. The linkage explained in this chapter is not about how sales revenue or an expense drives an asset, but rather how inventory drives its corresponding liability.

In our example the company purchases some products it sells and also manufactures other products. To begin the manufacturing process, the company purchases raw materials needed in its production ...

Get How to Read a Financial Report: Wringing Vital Signs Out of the Numbers, 8th Edition now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.