CHAPTER 14

CASH FLOW FROM OPERATING (PROFIT-MAKING) ACTIVITIES

Profit and Cash Flow from Profit: Not Identical Twins!

At this point we shift gears. Chapters 5 through 13 (except for Chapter 6) walk down the income statement. Each chapter explains how sales revenue or an expense is connected with its corresponding asset or liability. You can’t understand the balance sheet too well without understanding how sales revenue and expenses drive many of the assets and liabilities in the balance sheet. (In Chapter 3 we explain the increases and decreases of assets and liabilities in the recording of revenue and expenses.)

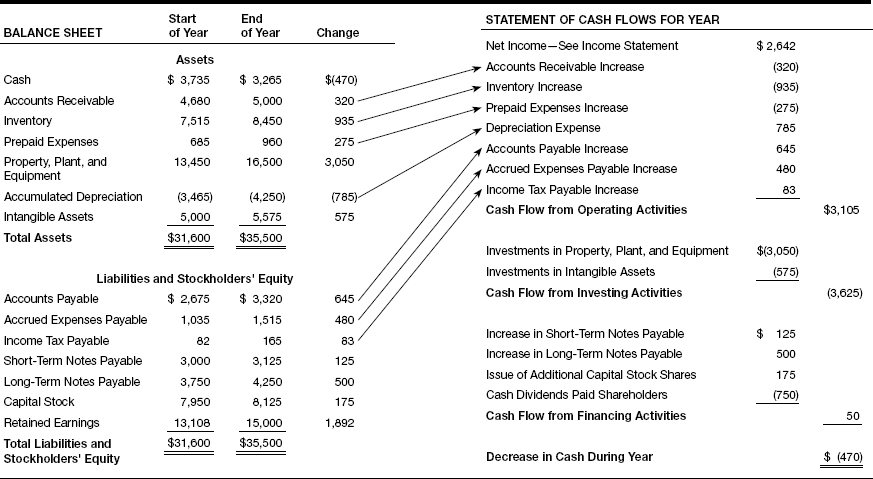

This chapter is the first of two that explain the statement of cash flows, which is the third primary financial statement reported by businesses in addition to the income statement and balance sheet. Exhibit 14.1 at the start of the chapter presents the statement of cash flows for the business we have discussed since Chapter 1. Please take a moment to read down this statement. We’ll make you a wager here. We bet you understand the second and third sections of the statement (investing activities and financing activities) much better than the first section (operating activities).

EXHIBIT 14.1—CASH FLOW FROM OPERATING (PROFIT-MAKING) ACTIVITIES

Dollar Amounts in Thousands

Exhibit 14.1 shows the balance sheets of the company at the start and end of the year and includes a column ...

Get How to Read a Financial Report: Wringing Vital Signs Out of the Numbers, 8th Edition now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.