CHAPTER 15

CASH FLOWS FROM INVESTING AND FINANCING ACTIVITIES

Rounding Out the Statement of Cash Flows

Please refer to Exhibit 15.1 at the start of the chapter. The preceding chapter explains the first of the three sections in the statement of cash flows, which without doubt is the hardest to understand. This chapter explains the other two sections of the cash flows statement, which are a piece of cake to understand compared with the first section that reports cash flow from operating activities.

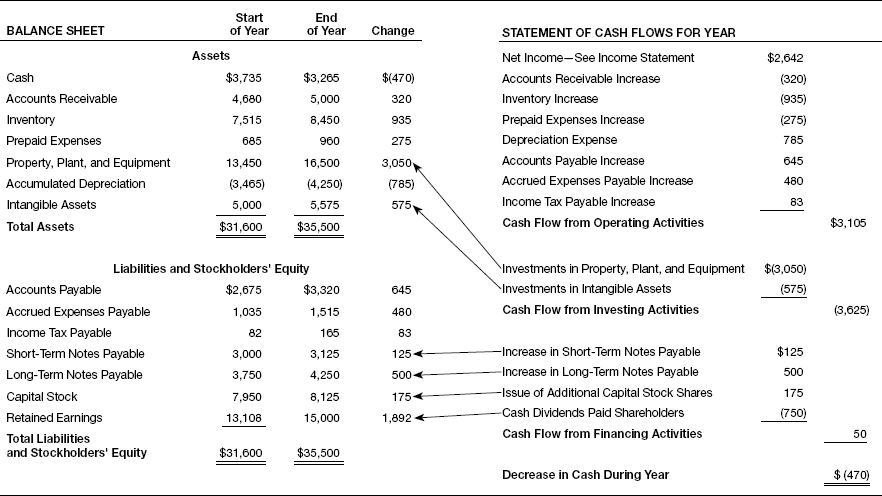

EXHIBIT 15.1—CASH FLOWS FROM INVESTING AND FINANCING ACTIVITIES

Dollar Amounts in Thousands

The second section of the statement of cash flows (see Exhibit 15.1) summarizes the investment activities of the business during the year in long-term operating assets. In the example, the business spent $3,050,000 for new fixed assets (tangible long-term operating assets). See the line extending from this expenditure in the statement of cash flows to the property, plant, and equipment asset account in the balance sheet. In addition, the business increased its investment in intangible assets $575,000 during the year.

The investing activities section also includes proceeds from disposals of investments (net of tax), if there are any such disposals during the period. In our example, the business did not dispose of any of its long-term operating assets during the year—tangible or intangible. We should ...

Get How to Read a Financial Report: Wringing Vital Signs Out of the Numbers, 8th Edition now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.