CHAPTER SEVEN

Integrated reporting

THE TOPIC OF INTEGRATED REPORTING, AND IMPORTANCE, was introduced earlier, particularly in Part II. This section expands on that in providing guidance and understanding as to the related notion and processes, and demonstrates its relevance in association with the preceding sections.

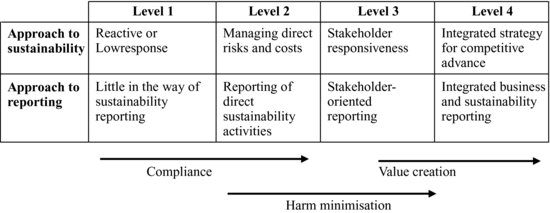

It is appropriate to identify why integrated reporting is worthy of attention. This is best done by relaying the key features and expected outcomes of integrated reporting – see Figure 7.1.

It is worthwhile reviewing the few points that constitute this presentation. As we can see, there are two main aspects:

- approach to sustainability;

- reporting approach.

As these aspects within a business entity, or any other organisation, rise in terms of collective responsiveness and responsibility, there is greater involvement of key stakeholders, as well as increased integration of strategy and reporting. The overall result of integrated reporting, therefore, is a movement from a position of mere compliance to one of value creation. Additionally, as is also evident at the very base of Figure 7.1, environmental harm is minimised, which is a beneficial outcome.

7.1 INTEGRATED REPORTING <IR>

Integrated reporting is a new approach to corporate reporting that demonstrates the linkages between an organisation's ...

Get IFRS and XBRL: How to improve Business Reporting through Technology and Object Tracking now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.