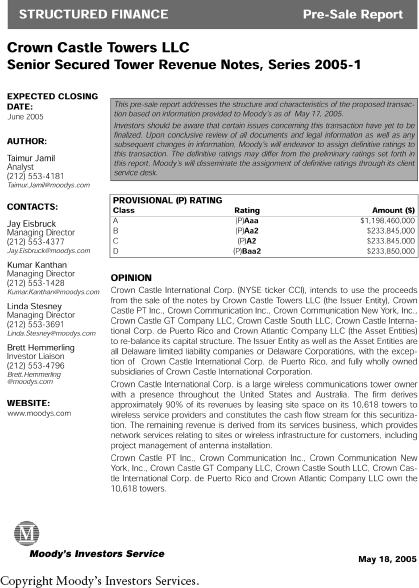

APPENDIX E

The Asset Entities were converted into special purpose entities and prohibited from having any employees, owning any other asset other than their own tower sites and from incurring any indebtedness other than the notes. The ownership of the towers was transferred via a True Contribution (“Sale”) of equity in the Asset Entities holding them to the Issuer Entity The bond holders will have a priority security interest in 100% of the equity interests of the Issuer Entity, The assets owned by the Issuer Entity through its 100% ownership of the Asset Entities include communication towers, real property and associated rights, managed and leased third-party sites, tenant leases, owned equipment on towers or at sites, FCC licenses and systems. Moody's ratings on this transaction are derived from our projected net cash that the pool will generate from leasing the tower sites over the life of the transaction, the structural enhancement including the subordinate tranches, and the legal structure.

Strengths

- The cross-collaterallzation of the large pool with diverse sites and locations reduces the volatility of the cash flows.

- Miscellaneous reserves accounts will be established including a Cash Trap Reserve Sub-Account that will become active should the DCSR fall below 1 75x over a trailing 12 month period at the end of any calendar quarter. In addition, if the DSCR falls below 1,45x ...

Get Introduction to Structured Finance now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.