ARIMA

ARIMA stands for autoregressive integrated moving average models. Generally, it is defined by the equation ARIMA(p, d, q).

Here,

- p is the order of the autoregressive model

- d is the order required for making the series stationary

- q is the order of moving average

The very first step in ARIMA is to plot the series, as we need a stationary series for forecasting.

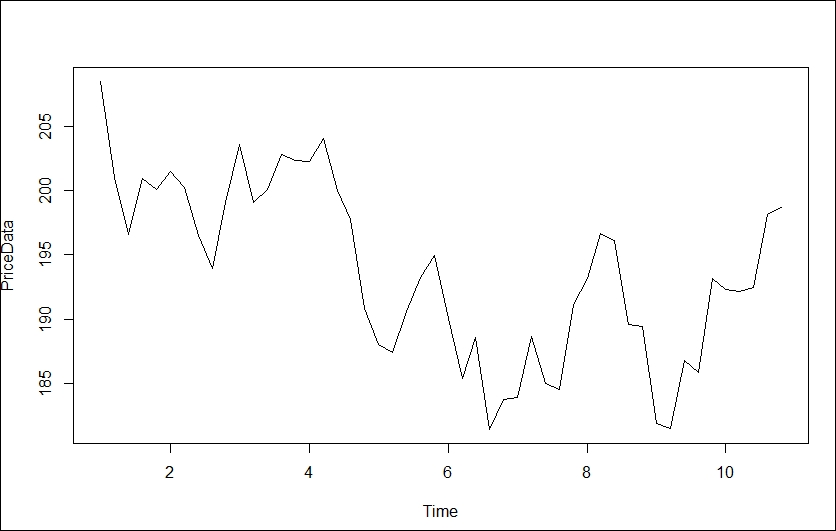

So let us first plot the graph of the series by executing the following code:

> PriceData<-ts(StockData$Adj.Close, frequency = 5) > plot(PriceData)

This generates the following plot:

Figure 4.9: Plot of price data

Clearly, upon inspection, the series seems to be nonstationary, so we need to ...

Get Learning Quantitative Finance with R now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.