Chapter 18

COST-VOLUME-PROFIT

CHAPTER LEARNING OBJECTIVES

After studying this chapter, you should be able to:

- Distinguish between variable and fixed costs.

- Explain the significance of the relevant range.

- Explain the concept of mixed costs.

- List the five components of cost-volume-profit analysis.

- Indicate what contribution margin is and how it can be expressed.

- Identify the three ways to determine the break-even point.

- Give the formulas for determining sales required to earn target net income.

- Define margin of safety, and give the formulas for computing it.

PREVIEW OF CHAPTER 18

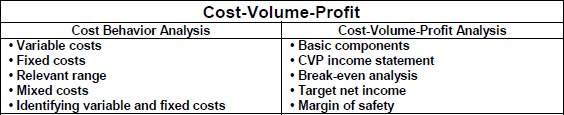

Management must understand how costs respond to changes in sales volume and the effect of the interaction of costs and revenues on profits. A prerequisite to understanding cost-volume-profit (CVP) relationships is knowledge of how costs behave. In this chapter, we first explain the considerations involved in cost behavior analysis. The content and organization of the chapter are as follows:

CHAPTER REVIEW

Cost Behavior Analysis

- Cost behavior analysis is the study of how specific costs respond to changes in the level of business activity. A knowledge of cost behavior helps management plan operations and decide between alternative courses of action.

- The activity index identifies the activity that causes changes in the behavior of costs; examples include direct labor hours, sales dollars, and units of output. ...

Get Study Guide Vol 2 t/a Accounting: Tools for Business Decision Makers, 5th Edition now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.