DOMAIN 3

Conducting Internal Audit Engagements—Audit Tools and Techniques (28–38%)

3.1 Data-Gathering Tools and Techniques

3.2 Data Analysis and Interpretation

3.1 Data-Gathering Tools and Techniques

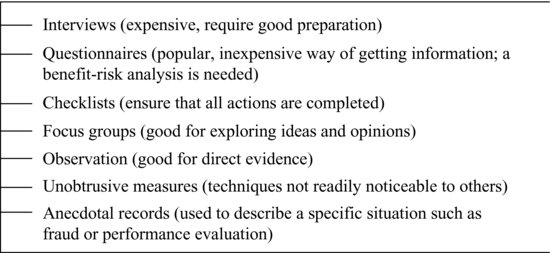

Auditors use several data-gathering tools and techniques to obtain background information on the auditee’s operations and to collect audit evidence and pertinent data for the audit purpose. Either statistical or nonstatistical sampling methods can be used to collect audit evidence and to control risk. Specific data-gathering tools and techniques include interviews, questionnaires, checklists, focus groups, observations, unobtrusive measures, and anecdotal records (see Exhibit 3.1).

Exhibit 3.1 Data-Gathering Tools and Techniques

(a) Interviews

(i) Types of Interviews

Interviews are of two types: structured and unstructured (i.e., less structured). A structured interview is one in which auditors ask the same questions of numerous individuals or individuals representing numerous organizations in a precise manner, offering each interviewee the same set of possible responses.1 In contrast, an unstructured interview contains many open-ended questions that are not asked in a structured, precise manner. With unstructured interviews, different auditors interpret questions and often offer different explanations ...

Get Wiley CIAexcel Exam Review 2014: Part 1, Internal Audit Basics now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.