Enterprise IoT: Overture

Where we are with enterprise IoT.

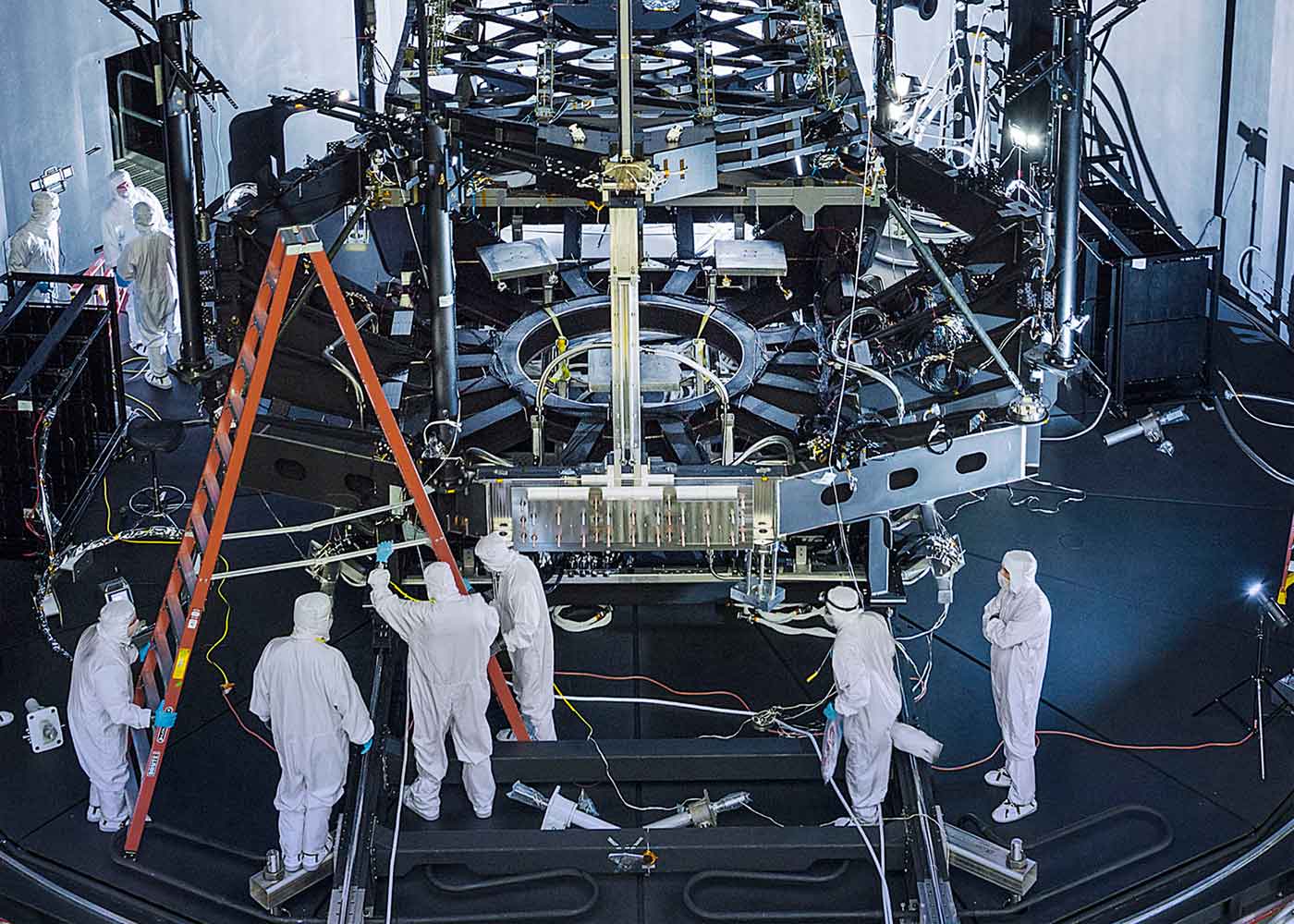

James Webb Space Telescope in NASA's giant thermal vacuum chamber. (source: NASA on Flickr)

James Webb Space Telescope in NASA's giant thermal vacuum chamber. (source: NASA on Flickr)

Mission: 50 Billion Connected Devices by 2020

If you did a Google search for “IoT” in 2012, the top results would have included “Illuminates of Thanateros” and “International Oceanic Travel Organization.” A search for “Internet of Things” would have produced a results page with a list of academic papers at the top, but with no advertisements—a strong indicator that in 2012, few people spent marketing dollars on the IoT.

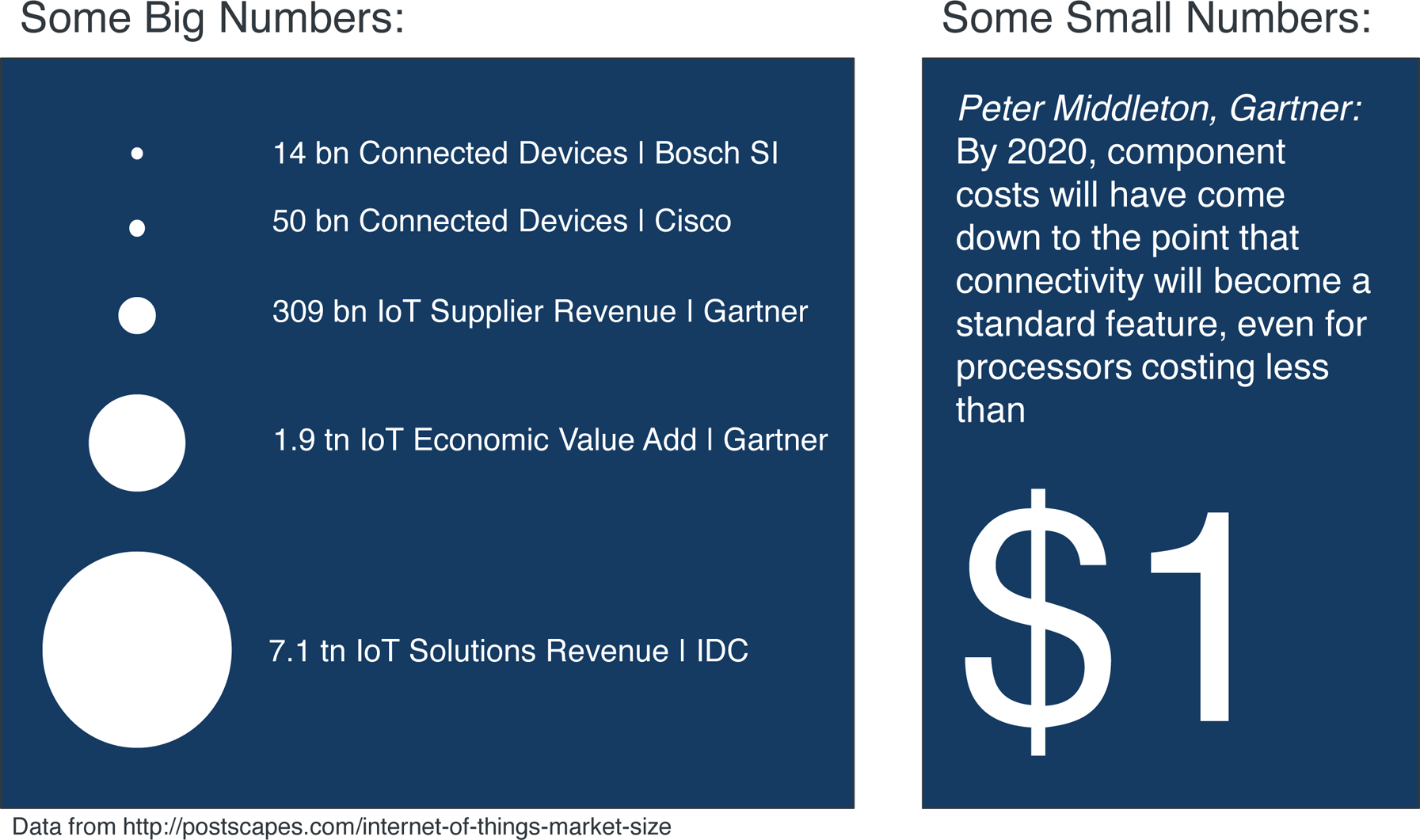

Two years on, and this had changed dramatically. In 2014, the IoT was one of the most hyped buzzwords in the IT industry. IT analysts everywhere tried to outdo each other’s growth projections for 2020, from Cisco’s 50 billion connected devices to Gartner’s economic value add of 1.9 trillion dollars (Figure 1-1).

Learn faster. Dig deeper. See farther.

Until we have reached this point in the future, no one can tell just how realistic these predictions are. However, the excitement generated around these growth numbers is significant, not least because it highlights a general industry trend while also creating a self-fulfilling prophecy of sorts.

We saw something similar happening with the auctioning of new mobile spectrum in the early 2000s. Literally billions were invested in the mobile Internet. And although it took longer than expected (remember the WAP protocol?), the mobile Internet eventually took off with the launch of Apple’s iPhone, and has since exceeded market expectations.

Meanwhile, Google—another major player in the mobile Internet sphere—has bet heavily on the IoT with its acquisition of Nest and Nest’s subsequent acquisition of DropCam. In addition, 2014 also saw many large IT vendors pushing themselves into pole position in the race for IoT supremacy, such as PTC with its acquisitions of ThingWorx and Axeda. On the industry side of things, many central European manufacturers and engineering companies rallied around the Industry 4.0 initiative, which promotes the use of IoT concepts in manufacturing. GE heavily promoted the Industrial Internet and spearheaded the establishment of the Industrial Internet Consortium. Many industrial companies began implementing IoT strategies and launching IoT pilot programs. And slowly the first real results emerged. Some were telematics or machine-to-machine (M2M) solutions dressed up as IoT solutions, while others were true IoT solutions according to our definition, which we will provide in not available.

Thus, at the time of writing, it seems that the final verdict on the significance of the IoT is still out. However, it looks as though industry is determined to seize the opportunities promised by the IoT. The authors of this book believe that the IoT (or whatever it will be called 5–10 years from now) will become as fundamental as the Internet itself. It took the Internet about 25 years to become as ubiquitous as television and the telephone system, and to transform a large number of industries. The situation in 2014 is reminiscent of the climate in the early 1990s, when we had our first exposure to Mosaic, and later Netscape, and the promises they stood for. Just think what a long way we have come since then, and where we stand with the IoT at the present time.

Customer Perspective: Value-Added Services

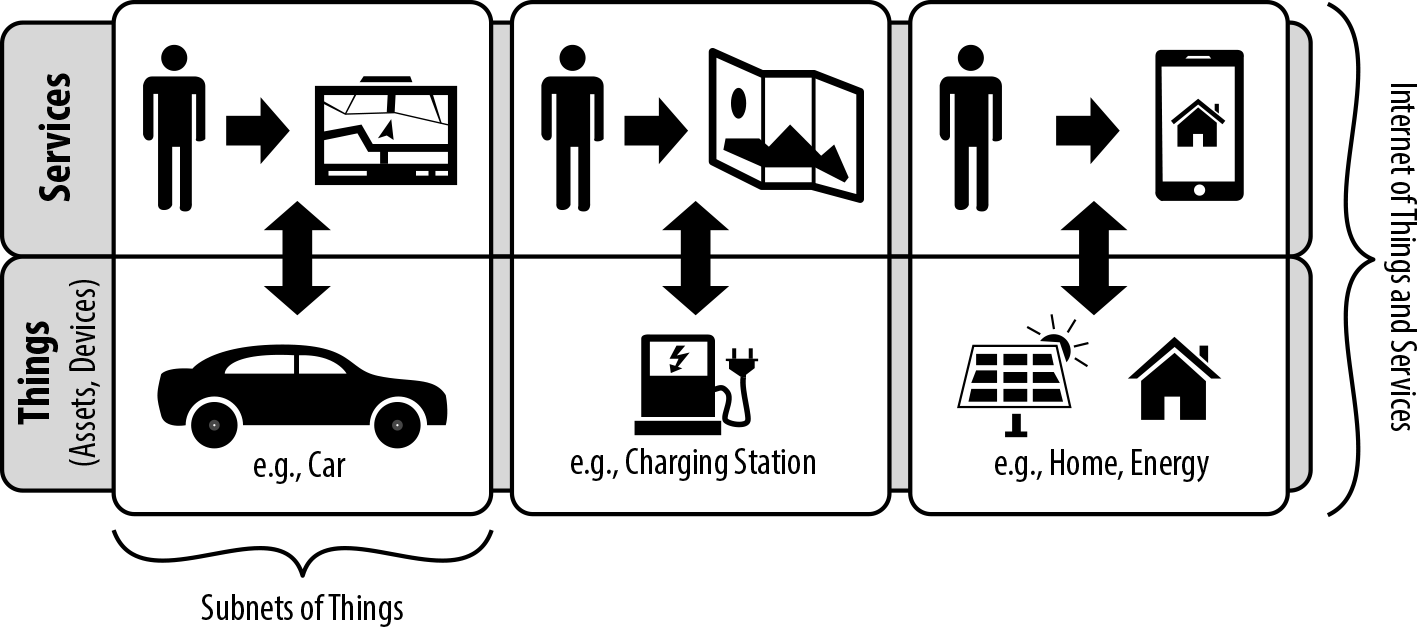

From the customer’s point of view, the main benefit offered by the IoT will be new services enabled by connected products and (potentially) backend services based on Big Data. Figure 1-2 provides an overview. Within different ecosystems (we call them Subnets of Things, or SoTs), assets (or devices that are part of an asset) are connected to a cloud or enterprise backend. New services are emerging with software running both on the asset and in the backend. For example, the Connected Horizon [BoschCH14] is a technology that has been developed by Bosch. It provides a backend that combines traditional map data with additional data such as traffic signs and road conditions, and then uses this data in the car to provide the driver and the vehicle’s various control devices with important advance information that enables safer driving. This is a good example of an SoT that already integrates a multitude of devices and external data sources.

Integration between different SoTs can occur at multiple levels. Assets can communicate with each other directly (e.g., in Car2Car, Car2X, etc.), or alternatively, integration can take place in the backend (e.g., Cloud2Cloud, Cloud2Enterprise, etc.)

For the end user, the advantages are value-added services based on connected assets and devices. Big Data can provide contextual information, as seen in the Connected Horizon example. Furthermore, Big Data analytics can be used to initiate additional customer services, such as recommendations based on customer profile and current location. There is no shortage of ideas for new business models based on these new technological capabilities.

Manufacturer Perspective: Connected Asset Lifecycle Management

From the manufacturer’s point of view, the potential impact of the IoT is equally as vast. Most manufacturers today hear very little about their products once they leave the factory. In fact, this was traditionally seen as the best possible outcome, the most likely alternative being a costly product recall.

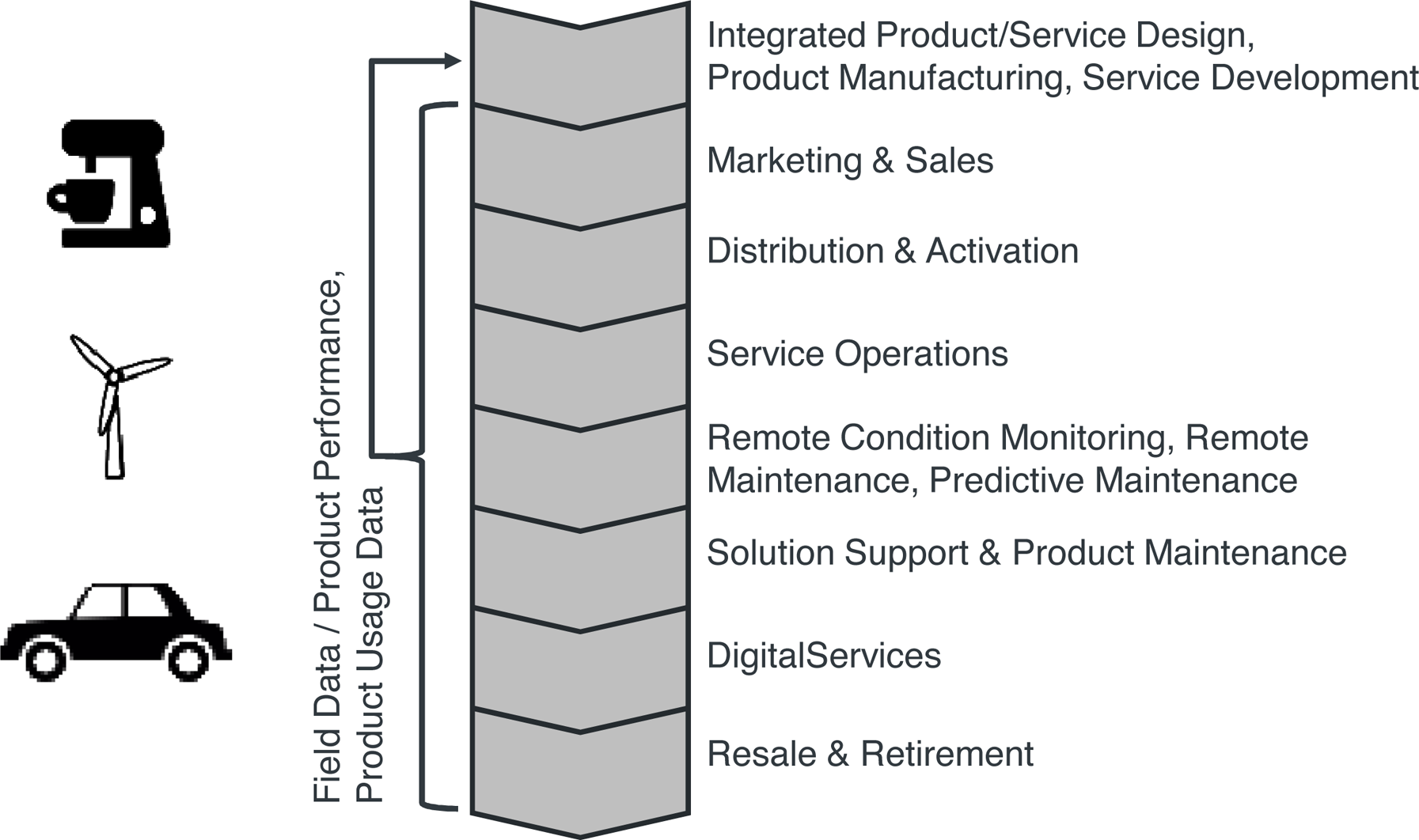

The ability to connect (almost) any kind of product to the IoT has the potential to fundamentally transform the value chain of product manufacturers. The traditionally disconnected asset lifecycle will become a fully connected asset lifecycle (Figure 1-3).

As we will discuss throughout this book, the capabilities provided by the IoT require a new appraisal of product design. How can new products leverage these new capabilities? How can value-added IoT services be created based on existing physical products? How can data received from connected products be used to optimize product design? How can we reconcile the different development times typically found in the worlds of physical products and software services? How can we align diverging development models (e.g., a Waterfall model for physical products and an Agile model for software services)?

New real-time and long-term analytics of usage data from connected products on the demands and behavior of product users will also have a dramatic impact on sales and marketing, as it provides new insights into usage patterns and value creation. Moreover, the IoT also has the potential to fundamentally change business models and value propositions, by moving from an asset-centric transactional sales model to a relationship-oriented service model, for example. In turn, this will require new organizational capabilities in sales and marketing.

Connected products also call for specialized processes for product or service activation, including the enablement of basic communication features (e.g., the activation of embedded SIM cards) as well as user account setup and management, and so on.

Following product activation, new remote-monitoring capabilities can be leveraged both by the service and the sales organizations. Particularly for industrial products, the use of remote condition monitoring in order to provide customers with advance warnings about potential problems, thus increasing Overall Equipment Efficiency (OEE), can be an important value add. Internally, product/service processes can be optimized by leveraging the same data. Analysis of product usage patterns could potentially help sales teams identify cross- and up-selling opportunities.

More than anything else, the combination of physical products and digital services has the potential to generate significant revenue after the sale of the initial product or service. Consider, for example, a service that allows customers to upgrade the engine performance of their cars for a weekend trip by temporarily reconfiguring the engine software.

Finally, connected products also make it easier to get involved in product resale and retirement activities, which is important from the point of view of customer retention.

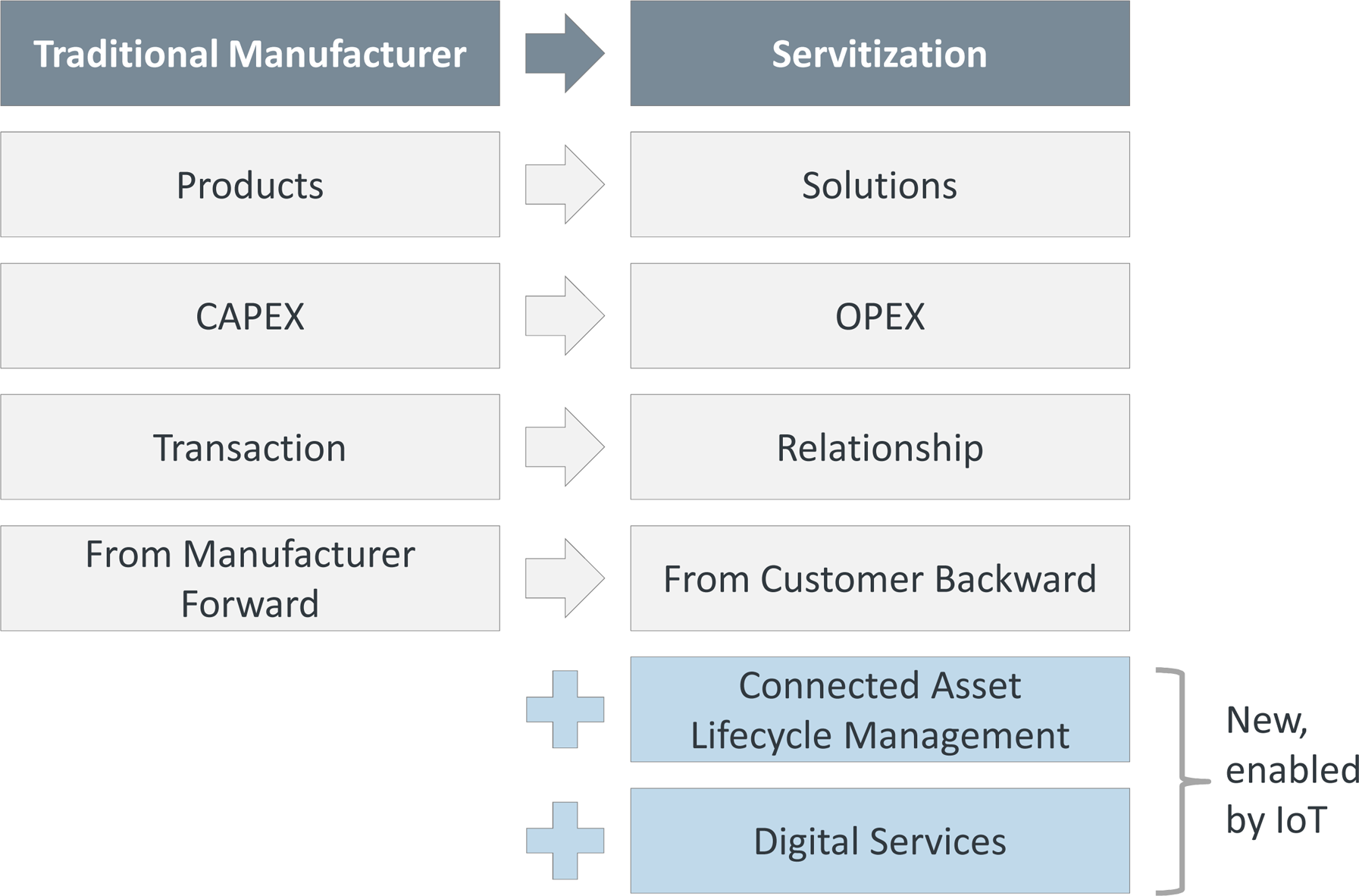

Servitization: The Next Logical Step?

Taking things one step further, many people in the IoT community see servitization as the next logical progression in the evolution of the IoT. The concept of servitization has been around since the late 1980s [Van88], but is currently experiencing a boost thanks to new capabilities such as connected asset lifecycle management.

The basic idea of servitization is that manufacturers move from a model based on selling assets toward a model in which they offer a service that utilizes those assets. For example, Hilti offers a service that guarantees customers access to required power-tool capabilities for as long as they are needed, wherever they are needed. The monthly fee—which includes costs for tool provisioning, service, and repairs—makes financial planning much easier for customers. Similarly, Rolls-Royce, GE, and Pratt & Whitney offer aircraft engines as a service (for a fixed rate per flying hour). One immediate benefit of such models for customers is that instead of earning money for each repair, suppliers are now highly incentivized to reduce the need for repairs, because they have to carry the costs themselves. And fewer repairs means greater uptime for customers. In addition, customers can focus on their core competencies, such as running an airline. Finally, a recent study shows that servitization customers are reducing costs by up to 25%–30% [Aston14].

From a supplier perspective, servitization also has many benefits:

-

Value-added services can generate additional revenue

-

Continuous, service-based revenue streams allow for more predictable financial planning

-

A recent study [Aston14] shows that servitization promises sustained annual business growth of 5%–10%

-

Highly differentiated services increase competitiveness

However, servitization does not come for free. Many manufacturers are focusing on product features and capabilities instead of taking a customer perspective focused on outcomes (Figure 1-4).

Instead of focusing on products, the focal point of servitization must be solutions. Instead of emphasizing output, suppliers need to take a customer perspective and think about results. Single sales transactions are converted into long-standing customer relationships. All this requires numerous changes—from strategy and business models to technologies and organizational setup.

As already mentioned, servitization is not a new development, and has been successfully deployed outside of the IoT. However, the IoT is now adding interesting capabilities that could help make servitization more efficient, or even pave the way for servitization models that were previously unfeasible:

-

The previously discussed concept of connected asset lifecycle management provides new insights into product usage, which can be leveraged to make servitization much more efficient for the supplier—for instance, by using remote condition monitoring instead of costly onsite equipment checks.

-

New IoT-based digital services could create completely new service models, in which a predictive maintenance solution can be used to sell improved service-level agreements (SLAs) with greater guaranteed uptime, for example.

Prerequisite: Operator Approach

All of the approaches just discussed—from connected asset lifecycle management to servitization—have a common prerequisite: manufacturers must adopt an operator approach in order to implement them successfully. This is something that should not be underestimated, because it requires a completely different infrastructure, organizational setup, and set of processes from those found in a traditional manufacturing business. Operating an IoT-based service is not just a technical challenge; operational considerations can go far beyond the operation of an IT service infrastructure.

For example, the eCall service discussed later not only requires the operation of an IT infrastructure that can accept and process incoming distress signals from vehicles on the road; it also requires a physical business operation, mainly in the form of a call center that can receive incoming distress calls from drivers and ensure that these calls are answered in the right language, among other considerations.

Another example is provided by the real-time car-sharing services that we will discuss later. These services need an efficient fleet management process and service structure, which a manufacturer may not be able to establish and operate alone. For instance, it is no coincidence that BMW set up a joint venture with car rental company Sixt to operate the DriveNow service. It is clear that BMW is relying on Sixt’s experience in operating a very large fleet of rental cars and car rental stations and in managing customer relationships.

Another interesting industry with a wealth of operator experience that may be hugely relevant to the IoT is the telecommunications industry. Few other sectors have as much experience in running an organization and infrastructure that supports millions of distributed, intelligent, connected devices with advanced backend services. Moreover, this industry has a great deal of experience in managing firmware and application updates for remote devices such as smartphones.

For companies striving to conquer the IoT, it will be vital to learn from these kinds of examples in their transition toward becoming service operators.

Impact: Disruption Versus Evolution

We believe that the IoT has the potential to disrupt many industries in the future, just as the Internet did over the last few decades. Take as an example real-time car-sharing services. A number of companies (e.g., DriveNow, Car2Go, and ZipCar) are now offering customers real-time car-sharing services. Instead of owning a car, customers can simply locate and reserve the nearest available car using an app on their smartphone, open the car with a chip card, use a specialized onboard unit in the car to manage the rental process, and simply lock and leave the car once they have reached their destination. Currently, these services are mainly limited to urban areas. However, with many young urban consumers no longer viewing a car as the ultimate status symbol, these kinds of services are becoming increasingly popular and have the potential to transform the entire automotive industry over the coming decades.

Another potential disruptive aspect of the IoT concerns data-driven business models in formerly asset-centric business areas. Google’s Nest giving away thermostats for free, and then earning money by means of houseowners’ behavior profiles, would be one example. Another scenario goes back to the example of car sharing. Imagine your service provider offering you 50% off the cost of a ride if you agree to listen to targeted advertisements while you drive. Combining your customer profile data with location-based information could be very attractive for local businesses eager to target you with special offers. In fact, this could even develop to the point where your local mall offers to sponsor your ride entirely, provided you use the car to drive to that specific mall. If we then add autonomous driving to the mix, the automotive industry will be changed beyond recognition, as it will truly have transformed into a transportation business.

There are many other examples of potentially disruptive business models driven by the IoT, from smart grids to smart homes and smart cities. However, a number of obstacles will also need to be overcome, including regulatory requirements (e.g., a lack of regulation permitting autonomous driving), an absence of standards to allow interoperability, and the complexity of some of the technologies required for some IoT applications.

Finally, not all use cases supported by the IoT are necessarily disruptive. Many companies today are looking at more evolutionary use cases—including remote condition monitoring (RCM), remote maintenance, and predictive maintenance—as well as highly specialized service add-ons for existing assets, such as the eCall Service, which notifies emergency services in the event of a car accident.

The important and potentially huge impact that these more evolutionary IoT-based servitization use cases will have on existing organizational structures should not be underestimated. Transforming a large service and support organization to make efficient use of remote services such as remote condition monitoring and remote maintenance will unquestionably require significant organizational change, and it may well take a number of years before the positive effects of these new capabilities are fully leveraged.

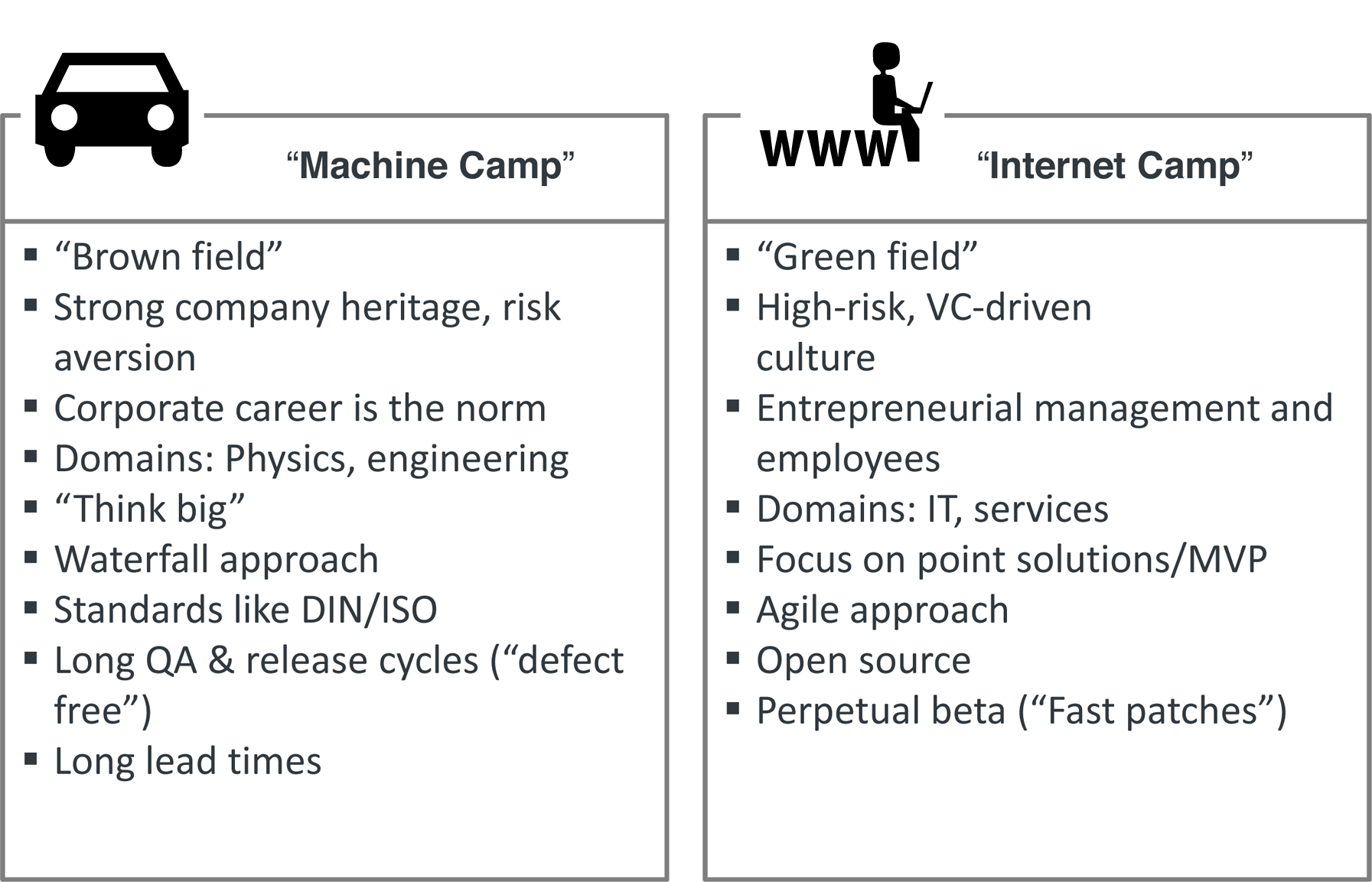

Clash of Two Worlds: Machine Camp Versus Internet Camp

As exciting as the opportunities presented by these “connected products with services” are, we need to bear in mind that they will require two fundamentally different worlds to work together: the physical world and the service world. And this is not as easy as it sounds.

The physical world has traditionally been dominated by what we will refer to (for simplicity’s sake) as the “machine camp”: manufacturers, engineering companies, and so on (Figure 1-5). On the other hand, we have the “Internet camp”: companies that have, over the last 25 years, rapidly transformed several industries with their Internet-based service offerings.

Most people in the machine camp work for companies that have a long heritage, some with roots in the early Industrial Revolution. To achieve such long-term success, careful risk management and long-term strategic thinking is paramount. Those in the Internet camp, on the other hand, usually start on a green-field site without the restrictions of existing product lines that must be maintained, or corporate governance rules that must be followed, and often with extremely big risks. The venture capital (VC) funds often backing these companies actually demand such high-risk/high-growth strategies. The VC business model is typically based on the assumption that only a small number of investments will succeed, but those that do will pay such a high dividend that it is acceptable to write off other failed investments (an approach described as “fail fast, fail often, fail cheap”).

This also has a strong impact on corporate culture in these different environments. In the machine camp environment, a corporate career is the norm. Many managers will move between vastly different domains and roles over the lifetime of their career. This can lead to situations in which a longer learning curve is required in a new job. Members of the Internet camp are often more focused on subject matter, and tend to follow their passion rather than a long-term career development plan. This can be advantageous, in that they will push a project they strongly believe in much harder. On the other hand, many entrepreneurs generally tend to stay with a company during a specific phase only, often the early-growth phase.

Many of those in the machine camp have a background in physics or engineering, while the domain of the Internet camp is often IT and services—two key perspectives that need to be combined in the IoT world. Because of their background, people in the machine camp tend to think big in terms of complexity of solutions and global rollout (e.g., for cars, aircraft, or steel mills). The Internet camp usually also thinks big in terms of global rollout, but often starts with very focused point solutions (e.g., Skype, WhatsApp, Doodle, etc.) that evolve over time into more complex platforms (e.g., Amazon, eBay, or Salesforce.com). The concept of the minimum viable product (MVP) has become a common strategy for many startups, promoting an iterative process of idea generation, prototyping, field trial, data collection, analysis, and learning.

Another key difference that must be bridged in the IoT is the general approach to running projects. Many in the machine camp still run projects using a Waterfall model, while most in the Internet camp have by now adopted An agile approach. For many Internet companies, following a perpetual beta approach is the norm (“fast patches”). Large Internet portals commonly roll out multiple updates per day, often running test versions for smaller user groups in parallel. Those in the machine camp come from a world where a single failure can have potentially deadly consequences (e.g., malfunctioning car brakes) or, at the very least, result in costly and image-damaging product recalls. Naturally, therefore, lengthy QA and release cycles are the norm in this environment, the aim being “zero defects.”

This is perhaps one of the biggest challenges for the IoT. However, it is clearly influenced not only by cultural differences, but also by technological restrictions. For decades, the machine camp had to deal with environments in which it was nearly impossible—or was otherwise cost prohibitive—to modify a product after it had been deployed in the field. With the ever-increasing digitization of products in the IoT, this is now changing. For example, it is now possible to remotely update the embedded software that controls a car engine. Of course, we are not suggesting that the perpetual beta approach should be applied to car engine control software. However, it is clear that there are many benefits to this new flexibility—for instance, the ability to simply roll out two million patches over a global, wireless network instead of having to recall two million products. Yet in order to take advantage of the new opportunities offered by digitized physical products, manufacturers will have to transform themselves into operators that are capable of managing these processes in a secure and highly reliable way. Incidentally, a lot can be learned from the telecommunications companies and smartphones platform operators here, as they are currently the only ones who understand how to operate networks comprising millions of intelligent, physical products and how to deal with issues such as software updates on this scale.

The pressure is on for many of those in the machine camp in this area. Customers do not understand why they can update their smartphone apps at the tap of a finger or purchase a new generation of powerful smartphone every year, but are stuck with their cars’ onboard systems for years on end without the option to update hardware or software, or at least not easily. Nobody wants to spend an afternoon at the auto repair shop installing the new telematics unit required for a new, usage-based insurance (UBI) policy. Customers want the same experience they receive from their smartphones: “Do you want to allow the ACME Insurance app to access your driving behavior? Click ‘yes’ and save $100 a year on your car insurance.”

Of course, the differences between the machine camp and the Internet camp are not just cultural or technological in nature. Another important area relates to standards and regulatory requirements. Those in the machine camp are accustomed to living in a world dominated by DIN, ISO, and the like. Whereas those in the Internet camp often take the liberty of ignoring these restrictions, especially in early development phases. Take, for example, the development of a truck fleet management solution with an integrated telematics unit. Regulations in different countries require the communication modules to use different frequencies. A startup might simply ignore this requirement and take the risk of rolling out a solution based on a single frequency in different countries, which may mean capturing markets faster, but at a higher risk. A large company simply cannot afford to take such a risk, and will attempt to build a multifrequency solution from the beginning. This means the solution will be much more complex to start with, and will probably be rolled out later and possibly at a higher cost. Managing such situations while also balancing cost efficiency and compliance is a key challenge for large companies, particularly in the context of the IoT.

Every company will need to find its own way of dealing with this “clash of two worlds.” Some may try to build bridges and new capabilities internally; some may seek out partners; while others may decide to go down the acquisitions route. There are many different examples in practice, from Google’s acquisition of Nest, to BMW’s joint venture with Sixt for the new DriveNow car-sharing service.

Difficulty of Finding the Right Service

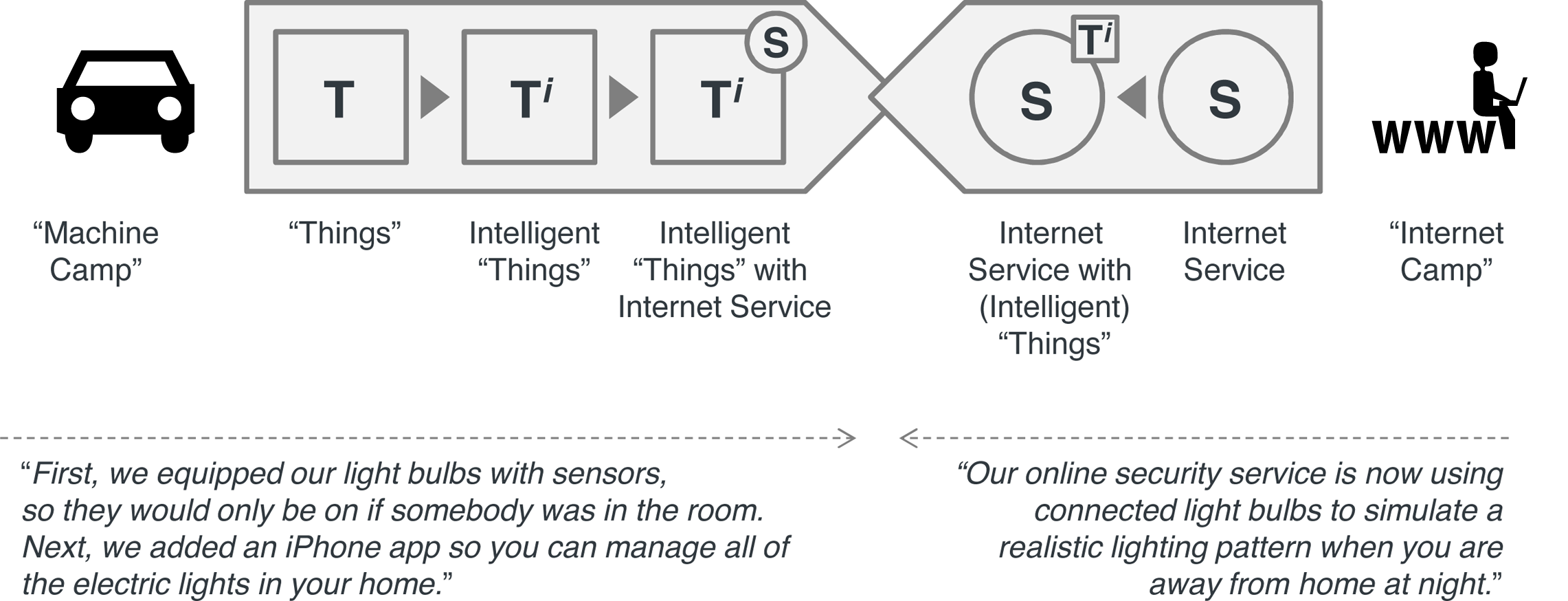

As we can see, bringing together the worlds of the machine and the Internet in the context of a single solution is challenging at the very least. Furthermore, in our experience, it is quite common for the development of an IoT solution to have one of the two perspectives as its starting point—i.e., either the Internet camp moves toward the physical world, or the machine camp moves toward the service world (Figure 1-6). Over the past few decades, the machine camp has transitioned from “things” to “intelligent things” by adding local intelligence using electronics. Now many are adding connectivity, and moving toward what we call “intelligent things with Internet services.” The Internet camp, on the other hand, started off with Internet services, and is now moving toward “Internet services with (potentially intelligent) things.” This means that we are essentially looking at two different versions of the same IoTS formula: one has a “thing” at its root, the other a service.

Let’s discuss the implications using a theoretical (and again exaggerated) example (inspired by [HSG14]): remote-controlled lightbulbs. In general, lightbulbs are a domain that has been dominated by the machine camp for the best part of a century, with high production volumes and usually low margins. Roughly 20 years ago, an interesting innovation took place whereby manufacturers added intelligence to lightbulbs by using motion detectors to switch on lights whenever movement was detected. And now we have the connected lightbulb, enabled by the IoT. So the question is: what happens if you ask people who have spent the last 20 years as a product manager for lightbulbs, focusing on improving things like energy consumption and product durability, to design a service that utilizes the new connectivity features? Our bet is that their immediate reflex would be to design a service that allows you to manage all of the lightbulbs in your home using your smartphone.

And what about the Internet camp? We expect that initially, they would not be interested, because remote management for lightbulbs is not the focus of their attention. But then one person in the Internet camp, who provides an Internet-based security service for homeowners, may pause and reconsider. What if you recorded the homeowners’ light usage patterns and then played them back while they’re on vacation? That way, the remote-controlled lightbulbs could be used to improve the security service by simulating the lighting pattern that would occur if the owners were at home.

Let’s compare the two approaches. For the lightbulb manufacturer, adding the remote management service seems to make sense. The only question is this: will they be able to sell this service as a value add, and thus generate extra revenue? Or will customers simply assume this to be a standard feature of next-generation lightbulbs? Now take the security service that utilizes lightbulbs to provide an additional feature for a highly differentiated product. In this case, it seems more likely that the service owner will be able to charge extra for this feature, due to its innovative nature and the different context in which it is sold. However, they have no control over the technology used, and may run the risk of annoying their customers if the mechanism does not function properly—for example, if the lights stay on for the entire duration of the vacation, running up a big electricity bill. In summary, this means that we have two versions of our simplified IoTS formula for success:

-

Intelligent Thing(s) with Service: Ti + S

-

Service with Intelligent Thing(s): S + Ti

This example may not be perfect, but it helps to highlight some of the key points about the differences in thinking with regard to IoT business models. Many believe that truly transformative, IoT-enabled business models will require more out-of-the-box thinking in respect of new services, as our example demonstrates.

As outlined earlier, there are many other differences in the typical behavior of engineering-based companies versus Internet-based companies. Engineering companies would be well advised to adapt certain elements of the startup world, such as service thinking and a bit more of a “fail early, fail often” philosophy. Internet companies, on the other hand, will not succeed in the IoT unless they learn from engineering companies about how to ensure high product quality standards and integration with the lifecycles of nondigital products.

Foundation: Digitization of the Physical World

The foundation for the new business models enabled by the IoT is the digitization of the physical world. Billions of sensors that generate massive amounts of information, cost-effectively managed by utilizing state-of-the-art, scale-out, Big-Data architectures, provide the basis for new Internet-based services. Cost efficiency is probably the key word here; from telematics to M2M, connecting sensors and other components with backend databases is not a new phenomenon. However, as outlined earlier, previous solutions were costly and limited in both scope and functionality. Advances in technology such as processors for mobile devices, (almost) ubiquitous wireless communication infrastructures, scale-out cloud data management, and the emergence of IoT application platforms now seem likely to bring down the cost of creating a real-time digital image of the physical world to a level that will allow the emergence of several new data-driven business models. Of course, there won’t be just one digital model of the entire physical world—we expect many different digital models to emerge, motivated by different use cases, company boundaries, partner ecosystems, and other parameters. We also expect these different digital models to develop along the lines of the Subnets of Things, which we described earlier. Using mashup technologies, different isolated digital models can be integrated to form more complex models that also help advance the transition from Subnets of Things to the IoT. These real-time digital models of the real world, enabled by sensors and Big Data, will provide the foundation for numerous different use cases, many of which are not even known yet.

Critical: Security and Data Privacy

The excitement surrounding digital models of the physical world, including the collection of new customer usage data and product data, also creates concerns for many users—and rightly so. Security is one such concern. Not only do we need to ensure that all of this “big” data in the backend is managed in a secure fashion; in a distributed environment such as the IoT, we need to secure the connections between the different participants, as well as the hardware and software running on the assets. Stuxnet [ST1] and the hacking of the Tesla Model S electric car [TH1] by Chinese students in 2014 illustrate just how important this issue will become. Imagine a hostage situation where criminals hacked into a pacemaker, or seized control of an aircraft in flight…

The other side of the equation is less concerned with external intruders and hackers, and more focused on the corporate policies and governance processes regulating the newly obtained customer and product data. One aspect here is compliance with regulatory and legal requirements in different countries. Another aspect is transparency and respect for customer rights and preferences. Many users rely on social networking services such as Facebook and LinkedIn to use their social media data to generate relevant updates and recommendations. However, these same users are frequently frustrated by the complex and ever-changing data usage policies enforced by such companies.

Given the nature of the data that could potentially be acquired by IoT solutions—not just social data submitted more or less voluntarily, but data captured by possibly hidden sensors and vital systems—it will be absolutely essential for the IoT industry to efficiently handle security and data privacy. Otherwise, there is a huge risk that customers will not accept these new IoT solutions, out of fear of an Orwellian dystopia.

Timing: Why Now?

Finally, many people ask: Why now? We have been waiting for hockey-stick growth curves in the M2M market for nearly a decade; why is the IoT taking off now? The answer to this question has partly to do with momentum, partly with business models, and partly with technology. In 2014, we could see that the IoT had gathered a momentum not shared by M2M. Business magazines like Forbes and Der Spiegel dedicated lengthy articles to the topic, creating a high level of visibility. Many large businesses have now instructed their strategy departments to devise IoT-based business models—even if we are still in the learning phase in this respect. Initial business successes can be seen, with examples such as ZipCar, DriveNow, and Car2Go. Most large IT players now offer dedicated IoT implementation services, IoT middleware, or IoT hardware (or a combination of all three). Finally, a combination of different technologies seems to have reached a point where managing the complexity of IoT solutions has now become more feasible and cost efficient:

- Moore’s law

-

Ever-increasing hardware performance enables new levels of abstraction in the embedded space, which provides the basis for semantically rich embedded applications and the decoupling of on-asset hardware and software lifecycles. The app revolution for smartphones will soon be replicated in the embedded space.

- Wireless technology

-

From ZigBee to Bluetooth LE, and from LTE/4G to specialized low-power, wide-area (LPWA) IoT communication networks—the foundation for “always-on” assets and devices is either already available or in the process of being put in place.

- Metcalfe’s law

-

Information and its value grow exponentially as the number of nodes connected to the IoT increases. With more and more remote assets being connected, it looks like we are reaching a tipping point.

- Battery technology

-

Ever-improving battery quality enables new business models, from electric vehicles to battery-powered beacons.

- Sensor technology

-

Ever-smaller and more energy -efficient sensors integrated into multiaxis sensors and sensor clusters, an increasing number of which are preinstalled in devices and assets.

- Big Data

-

Technology that is able to ingest, process, and analyze the massive amounts of sensor-generated data at affordable cost.

- The cloud

-

The scalable, global platform that delivers data-centric services to enable new IoT business models.

While nobody knows for sure exactly how many billions of devices will be connected by 2020, it looks as though the technical foundation for this growth is maturing rapidly, inspiring new business models, and making this an extremely exciting space to work in.

Keynote Contribution: IoT and Smart, Connected Products

To conclude our Overture, we have included an interview with James (Jim) Heppelmann. He is the president and chief executive officer (CEO) of PTC and is responsible for driving PTC’s global business strategy and operations. Previous to his appointment as CEO, Mr. Heppelmann served as PTC’s president and chief operating officer, responsible for managing the operating business units of the company, including R&D, marketing, sales, services, and maintenance. He also serves on PTC’s Board of Directors.

Mr. Heppelmann has worked in the information technology industry since 1985 and has extensive experience developing and deploying large-scale product development systems within the manufacturing marketplace. Prior to joining PTC, Mr. Heppelmann was cofounder and chief technical officer of Windchill Technology, a Minnesota-based company acquired by PTC in 1998.

Mr. Heppelmann travels extensively to customer sites around the globe and speaks regularly at product development and manufacturing industry forums on topics such as the IoT, PLM, and gaining competitive advantage through product development process improvement. He has also been published and quoted in numerous business and trade media, including Harvard Business Review, The Wall Street Journal, and Bloomberg Television.

Dirk Slama: PTC has long been known as a leader in computer-aided design (CAD) and product lifestyle management (PLM). However, most recently you seem to focus a lot on IoT. Your acquisition of ThingWorx and Axeda alone must have cost you nearly a quarter of a billion dollars.

Jim Heppelmann: We see IoT as a disruptive force that will transform existing industries, especially in our core markets like manufacturing and engineering. PTC responded earlier to the growth of software-intensive products and service-oriented business models with hundreds of millions of dollars of investments in those key areas over the last 10 years. Adding connectivity to the product and service lifecycle solutions we already provide enables our customer to close the loop and transform the way they create, operate, and service their products. These investments will enable us to provide the best possible support for our customers in this critical transformation process, and certainly charts a course for PTC that is quite different from other CAD and PLM providers.

Dirk Slama: We have seen many M2M applications in the last couple of years that were focused on retrofitting remote condition monitoring (RCM)–like applications onto existing assets. Your vision for IoT-enabled products seems to go much further.

Jim Heppelmann: Such retrofitting approaches are important and will continue to play an important role for many established long-lived assets and products; however, we also see a new breed of products emerging that have been specifically designed to leverage the IoT. For these products, connectivity is not an optional add-on; rather, it is designed into the product. Many of the core features of these new products will rely on this built-in connectivity. Physical products and related cloud services are forming new ecosystems, like Apple devices and iTunes cloud services. We call this new breed of products “smart, connected products.”

Dirk Slama: So I assume that we need to rethink PLM for these smart, connected products?

Jim Heppelmann: Yes. Traditional PLM tools, in truth, really focus on the early stages of the product’s lifecycle—product design and development. We need to look at the entire product and service lifecycle, including product design, manufacturing, sales/marketing, customer operations, and after-sales services.

Dirk Slama: Let’s start with product design. What are the key issues here?

Jim Heppelmann: On the functional level, the product designers need to take a holistic systems engineering approach to design across the hardware and software layers of the physical product, and across the physical product and the related cloud services. Which new services can be enabled, and from where should they be enabled? And which existing functions can be optimized by leveraging connectivity—for example, by replacing clumsy onboard displays and buttons with a web interface that allows the operator or manufacturer to monitor, control, or configure the product from a new user interface, such as a smartphone? While enabling new capabilities, this approach dramatically increases the complexity of design and requires new design principles.

For example, to design for customization or personalization, designers need to capture the opportunity of hardware standardization through software-based customization. More and more of the variability of products today comes from the software layer, which drives down costs and enables customization later in the process. There is also a virtuous cycle here as innovations in the software layer drive increased value in the hardware, but hardware and software development have fundamentally different “clock speeds.” We might see 10 software releases in the time it takes to create one new version of the physical product on which the software runs.

This leads to another new design principle, designing for continuous upgrades and enhancements so that smart, connected products leverage connectivity for software upgrades throughout the life of the product. Design principles now need to anticipate opportunities to add or enhance product capabilities, and allow for these upgrades to occur remotely and in an efficient manner. Basically, the product becomes a platform on which increasing amounts of value can be delivered via software over time.

We also need to understand the new capabilities required in the development organization. Formerly siloed development teams need to interact much more closely, integrating the products’ hardware, electronics, software, and connectivity components. Agile software development processes need to be established and coexist with the more traditional hardware development cycles. New processes need to be defined to close the loop with product design. Direct, continuous, and often real-time data about how the product is being used will give engineering rapid feedback on how well their design functioned in the real world rather than simply using scenario-based simulation and testing. Value can be created from this data by using it to understand how to improve designs so that enhanced second and third generations of products are brought to market more quickly.

Dirk Slama: This also requires a new approach to sales and marketing?

Jim Heppelmann: Smart, connected products create new opportunities and reasons to transform your value proposition and even address completely different markets and refined customer segments.

This requires a different marketing approach and potentially new skill sets, too. The whole relationship with the customer is changing because companies are now able to stay in touch with the product after the initial sale. The product, in a sense, becomes a sensor for the relationship with the customer. Companies can gain amazingly detailed insights into the customer relationship by collecting and analyzing product usage data to understand how the product is performing, how much is it being utilized, which features are being used, and which features are not. This allows companies to improve segmentation, deploy more granular and targeted pricing models, deliver new, value-added services, and anticipate the needs of their customers. Recurring revenue streams can be created by combining physical products with digital content and services, which requires companies to transform the processes and culture across their marketing and sales organizations, and potentially their business models, to capture more of the newly created value. The implications of shifting from a discrete product sale to streams of upgrades and services over the product’s life are dramatic.

Dirk Slama: So “after sales” becomes “sales after the initial sale”?

Jim Heppelmann: Correct. Because products are now connected, we can stay in touch with the customer throughout the entire lifecycle of the product. This creates tremendous potential for cross-selling and up-selling. Take, for example, car engines. Instead of manufacturing multiple engines with different levels of horsepower, the horsepower rating on the same physical engine can be modified using software alone. By connecting this smart capability with a cloud service, a customer could upgrade his car for his weekend trip up the coastal highway; hence smart, connected products.

Dirk Slama: But traditional after sales services are still important?

Jim Heppelmann: Yes, of course. Product usage data can reveal current and potential future problems. Preventive and predictive maintenance are enabling product users and service organizations to prevent machine downtimes and improve overall equipment effectiveness (OEE).

For example, most service events today require multiple passes. The first pass enables a technician to identify the nature of the failure and what will be required to correct the problem; the second pass is to perform the actual repair. With smart, connected products, service technicians can obtain all “first pass” information remotely, and may even be able to perform the repair remotely if the failure can be remedied via software. The savings associated with reduced service calls can be substantial, and the product usage data can also be used to validate warranty claims and to identify warranty agreement violations, another huge expense for most product companies today. These approaches allow a manufacturer to transform its service business from reactive to proactive and create substantial gains in both service and operational efficiency.

However, this doesn’t come for free, and also has the potential to disrupt the high revenue, high profit service businesses that many companies have in place today. Service organizations that connect product condition and operations data with existing service processes can transform those processes, and potentially enable new processes and services that take advantage of the insights that come from the smart, connected products. By monitoring a product’s condition and proactively delivering service, sometimes via software, a company can improve the reliability and availability of the product. The potential benefits are significant, including reductions in field-service dispatch costs and capital costs for spare-part inventories. The threat of disruption comes if the benefit of the reduced need for spare parts and service visits accrues to the end customer, who then pays less for the cost of service. This reduced service demand may create a kind of “service paradox” for companies pursuing a smart, connected product strategy.

Dirk Slama: You recently coauthored the Harvard Business Review article “How Smart, Connected Products Are Transforming Competition” with Prof. Porter from Harvard Business School. In this article, you identified 10 strategic choices derived from the push toward smart, connected products.

Jim Heppelmann: The transformation ahead of many companies requires a clear definition of the goals and strategy in this area. A strategy requires trade-offs that create a unique competitive position, which has to be defined at the executive level and communicated to all relevant stakeholders. There is no right or wrong answer, only choices that must reinforce one another and define a coherent and distinctive overall strategic position for the company. Our framework of 10 strategic choices can help to define that company-specific strategy (Figure 1-7).

![10 strategic choices for IoT, based on HBR article by Jim Heppelmann and Prof. Porter [https://hbr.org/2014/11/how-smart-connected-products-are-transforming-competition/ar/1]](https://www.oreilly.com/content/wp-content/uploads/sites/2/2020/01/eiot_0107-15bf6ec9c8dc16f59174a25862d145bf.png)

The first set of questions is around the product and service strategy, starting with: Which capabilities should the company pursue? A smart, connected product drastically expands the number of potential product and service capabilities, but just because a company can offer many new capabilities doesn’t ensure there is sufficient value for customers above the incurred costs to the company. Next is how to best deliver those new product and service capabilities by determining how much functionality should be embedded in the product versus the cloud. Factors like required response time, expected network availability, complexity of the user interface, and frequency of service events or product upgrades will impact those decisions. The next set of questions is around the technology infrastructure required to enable smart, connected products. Developing the technology stack for smart, connected products requires significant investment in specialized skills, technologies, and infrastructure that have not been typically present in manufacturing companies. Some of the early pioneers like General Electric and Bosch have invested heavily via a largely in-house route to capture first-mover advantages and retain greater control over features, functionality, and product data. However, just as Intel has specialized in microprocessors and Oracle in databases, new firms that specialize in components of the smart, connected products technology stack are already emerging, and some in-house efforts may overestimate the ability to stay ahead, turning an early lead into a long-term disadvantage. A related question is whether the system architecture should be open or closed, where key interfaces are proprietary and only chosen parties gain access. While this has clear benefits for the company to control and optimize the systems, over time we expect closed approaches to become more challenging as technology spreads, ecosystems develop, and customers resist limits on choice.

Dirk Slama: The increasing focus on product data also requires a strategic take?

Jim Heppelmann: Yes, we see data and the insights derived from analytics becoming the key differentiator in a smart, connected world. This is really key to capturing the full opportunity. There are three strategic choices specific to data, first of which is: What data do I need? Capturing and analyzing data is fundamental to value creation, but also imposes costs and risks. Variable product costs increase from additional sensors, carrier-based data transmission, and so on, and fixed costs from robust analytics capabilities and skills required to translate Big Data into insight. And almost any data collected brings with it the risk and burden of data stewardship to ensure that all the data is secure and protected over time.

This relates to the next data choice around how the company manages ownership and access rights to the data. Firms must determine their approach to data ownership, sharing, and transparency. For example, providing data access to upstream component suppliers may improve component quality and innovation but may lead to new competitive threats if the supplier develops value-added services for the end customer using the data. The services that GE Aviation provides directly to airlines based on data collected from the aircraft engine is a real-world example for Boeing and Airbus.

This brings us to the third data choice about monetizing the data. Companies may find that the data they capture is valuable to entities beyond their traditional customers, creating new services or even businesses. The challenge is in defining mechanisms that provide valuable data to third parties without alienating existing customers or increasing regulatory risks.

Dirk Slama: All of these choices seem to open up some corporate-level decisions around the company’s business model and scope.

Jim Heppelmann: Yes, through the capabilities and data generated by smart, connected products, firms are now able to maintain direct and deep customer relationships through the products, which can reduce the need for distribution channel partners. Tesla Motors, for example, has disrupted the automotive industry by selling cars directly to consumers rather than through a dealer network. In an existing business, we would only caution not to underestimate the relationship that customers may have with existing channel and service partners.

Through those same capabilities, companies may be inclined to change their business model from product sales toward product-as-a-service. As customers pay for the performance of the product instead of the ownership of the asset, the value of the product improvements (like improving product quality or service efficiency) will be captured by the manufacturer.

Finally, as products continue to integrate in product systems and diverse networks, many companies will have to reexamine their core mission and determine what role they want to play in these larger systems; should they attempt to provide the platform and services for the entire system or play a supporting role in a broader industry landscape?

All difficult choices, but we believe that by providing the right strategic framework and ensuring the right environment for their execution, IoT and smart, connected products will be the foundation for the next era of IT-driven productivity growth for these companies and their customers.