Jean-Baptiste Raguenet, A View of Paris with the Ile de la Cité, 1763 (source: Digital image courtesy of Getty's Open Content Program)

Jean-Baptiste Raguenet, A View of Paris with the Ile de la Cité, 1763 (source: Digital image courtesy of Getty's Open Content Program) The Section High Alpha Pass is one of the slowest and most dangerous maneuvers performed by the Blue Angels, the United States Navy’s legendary flight demonstration team. The idea for the maneuver originated in 1992 with John Foley, then the team’s lead solo pilot. But it took weeks for the elegant maneuver—which requires two pilots to slow their F/A-18 Hornets to a few knots above stall speed and then pitch up to a steep angle at low altitude—to be perfected and integrated into the team’s air show routine.

“The maneuver had never been done with two airplanes. It’s scary enough doing it with one airplane,” says Foley. “The first step was proof of concept. We had to figure out the contingencies. What if something went wrong? What if one plane lost an engine? We had to go out and test it. You couldn’t test it in a simulator because no one had ever done it before.”

After Foley and his wingman had thoroughly tested the risky maneuver, they had to sell it to the rest of the team. “The hardest part was integrating the maneuver into the air show. We had to get the team to buy into it and we had to explain the purpose,” says Foley. “What’s really cool is that more than 20 years later, it’s still part of the Blue Angels air show.”

The Section High Alpha Pass, shown in Figure 1-1, is a textbook example of how innovation works in the real world. It wasn’t enough that Foley had a great idea; he had to prove it would work and then sell it to his organization.

Innovation = Invention + Value

“Innovation” is often used loosely to describe any kind of process for creating something new. From a strictly business perspective, innovation is customarily defined as the combination of invention and economic value. In other words, to be considered truly innovative, an invention needs to create new value.

Clayton Christensen, the “godfather” of modern innovation strategy, writes about two distinct forms of innovation, sustaining innovation and disruptive innovation, and it’s important to understand the difference.

The goal of sustaining innovation is gradual or incremental improvement of existing products or product lines. You’re making things better, but not rocking the boat. Sustaining innovation is slow, steady, and predictable. Institutional investors love it because it’s all about growth with manageable risk. Examples of sustaining innovation include new releases of software, new models of cars, and every new version of the iPhone.

The goal in disruptive innovation is creating not only new products, but also new business models and new markets. Disruptive innovation often appears rushed, risky, half-baked, and unpredictable—which explains why disruptively innovative new products and services are often dismissed, at least initially, as impractical or useless ephemera. Examples of disruptive innovation include Google, Amazon, YouTube, Facebook, Uber, and the original iPhone.

Most people have no problem understanding the idea of sustaining innovation; everyone likes better products. Disruptive innovation, on the other hand, can be polarizing and disconcerting. Disruptive innovators are regarded with a mixture of admiration, fear, and outright hostility. Early adopters of the newest tech loved Steve Jobs. But if you ran a company that was disrupted by one of Steve’s many innovations, you hated him.

Mapping the Innovation Landscape

Everyone, it seems, accepts the mantra that innovation is a key to success in competitive markets. But few organizations have developed the practical frameworks or detailed processes necessary for enabling steady flows of new products and services. Talking about innovation is easy; doing it on any kind of regular schedule is extremely difficult.

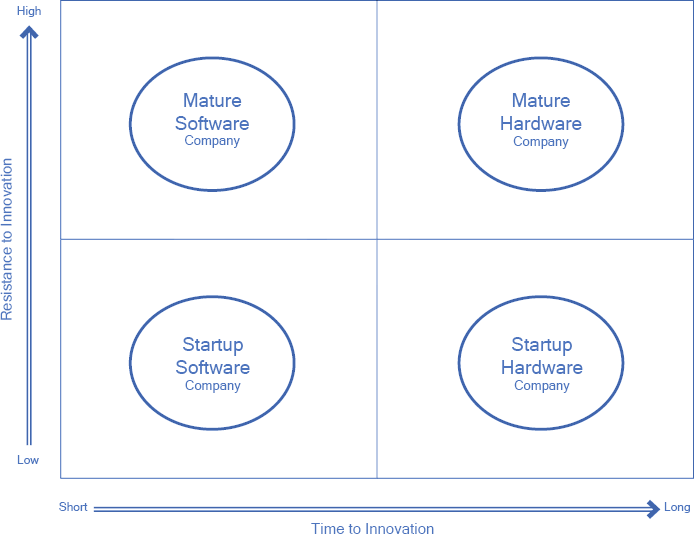

Small firms have less friction to overcome when innovating, but large firms usually have more cash for investing in R&D. They also have more legacy systems to deal with and more institutional baggage. If you’re the owner of a one-person shop writing software code, it will be easier to innovate than if you’re the CEO of a 100-year-old company that makes consumer package goods.

Figure 1-2 shows the rough relationships between types of business, resistance to innovation, and time to innovation. Innovation will encounter the most resistance and take the most time at a mature company that produces tangible goods. In other words, the more successful you are, the harder it is to innovate, especially if you make products from atoms rather than from electrons.

Pivoting to Greatness

Sometimes innovation results from a “pivot,” in which a company, usually a startup, suddenly realizes that a new product or service can be used in a way that was unforeseen by its creator. Slack is a great example of a successful pivot, says Jake Flomenberg, a partner at Accel Partners, which was an early investor in Slack. “It’s a classic pivot story,” says Flomenberg. “Slack began as a video game that didn’t get much attention. But the underlying communication infrastructure was actually pretty cool.”

The young company dropped the game and focused on developing the messaging platform, which evolved into Slack, a popular collaboration tool with more than a million active users.

Docker is another example of a technology product that pivoted to success. It began as an internal project within a platform-as-a-service company, dotCloud. Docker was released as an open source project in 2013, and it quickly became one of the most popular projects on GitHub. Today, it’s widely considered the essential “shipping container” for moving applications across multiple infrastructures in the cloud. Here’s another testament to its success: dotCloud has changed its name to Docker.

It’s natural for startups to rely on pivots, because there are often no alternative strategies. “A startup is trying to build one product,” says Flomenberg. “If the product doesn’t work or doesn’t get traction in the market, the startup is in trouble. The stakes are existential. They need to innovate or die.”

For a startup, pivoting is a legitimate form of innovation—and often the only available choice. Established companies with deeper pockets have more options for keeping projects afloat longer. In the end, however, the market decides which new products live and which die.

Or at least that how it’s supposed to work. Sadly, there are many examples of innovative products that were shelved or ignored by the company that developed them, simply because the products didn’t fit neatly into the company’s business strategy.

The laser printer, for example, was invented by a Xerox engineer named Gary Starkweather. But Xerox’s revenue model relied on selling high-priced products, and it effectively surrendered the mass market for laser printers to a host of competitors like Canon, HP, Brother, IBM, and Apple. The story of Xerox’s inability to capitalize on innovative technology it developed or helped pioneer—such as the mouse, the personal computer and the graphical user interface—has been the subject of many articles, including “Creation Myth,” written in 2011 by Malcolm Gladwell.

It’s Not Always About a Product

The takeaway isn’t that Xerox was run by idiots—it wasn’t—but that business model innovation is just as important as technology innovation. For example, we tend to think of GE as a company that makes products. I would argue that one of GE’s major contributions to global prosperity was its decision in the 1930s to extend consumer credit to millions of households. That was a business model innovation, and it helped the US consumer economy survive through the Great Depression.

Henry Ford is mostly remembered for inventing the automobile assembly line, but he also created a network of independent franchise dealerships that guaranteed a dependable source of capital for investing in new technologies.

IBM recently launched an Internet of Things for Automotive solution, a cloud-based service that helps automakers gather data from real-time sensors in the cars and trucks they build. Neither the sensor technology nor the analytics component of the solution is cutting-edge. What seems truly innovative about the solution, however, is its ability to compress data from the cars so network costs don’t go through the roof. “We can compress the data coming from the automobiles into very small, easy-to-ship packets that can be decoded on the other end,” says Chris O’Connor, general manager of IBM’s new Internet of Things unit. “Then it becomes a question of how much data do you really need and how are you going to analyze it.”

IBM is betting that automakers are sophisticated enough to understand the value of managing network costs as the IoT plays a larger role in their business ecosystems.

IBM’s ability to innovate an enterprise solution for a new market demonstrates one of the advantages that large companies have over smaller firms: big companies already have portfolios of existing products and services they can mix and match to create new solutions quickly and cost-effectively.

Larger companies also have expertise and depth in enterprise sales and marketing, which enables them to achieve scale with innovative products and services more rapidly than smaller competitors.

During World War II, Lockheed set up a semi-autonomous “skunk works” within the company to design and produce new aircraft at an accelerated pace. Led by Kelly Johnson, the Lockheed skunk works generated innovative airplanes such as the P-38 Lightning, the F-104 Starfighter, the U-2 Dragon Lady, and the SR-71 Blackbird.

Many companies have tried to follow the skunk works model, and have found it too difficult to replicate successfully in modern corporate settings. An exception to the rule is MasterCard Labs. Created in 2010 by MasterCard’s then chief operating officer, Ajay Banga, who is now the company’s CEO and president, MasterCard Labs has emerged as an engine of rapid innovation.

Since its inception, MasterCard Labs has developed a series of new technology products including Qkr!, a mobile payment ordering app, and ShopThis!, an online app enabling consumers to use a “Buy Button” for purchasing items while they’re reading an article or looking at an ad within a digital publication.

“In the past, development lifecycles were measured in years. Now, our goal is developing new product concepts in days or weeks,” says Betty DeVita, chief commercial officer at MasterCard Labs. “For us, innovation is a discipline and a driver. We’re looking beyond payments to commerce to understand what drives the overall digital space.”

Creating a separate unit specifically for innovation eliminates many of the distractions that often delay or derail projects in “business as usual” corporate environments. “Within MasterCard Labs, we focus on innovation,” says DeVita. “Our focus and our discipline allow us to deliver results using proof of concepts. That’s the key to unlocking the power of innovation.”

To help foster innovation outside of the organization, MasterCard Labs launched Start Path, a global effort to support innovative early stage startups developing the next generation of commerce solutions. More than 40 commerce-related startups, including Nymi, ZenCard, BillHop, and Gone, are now part of the program.

Different Rules for Hardware

From the beginning of recorded history until the closing decades of the 20th century, the concept of innovation has been tied closely to tangible inventions like spears, spurs, saddles, plows, looms, steam engines, automobiles, airplanes, and rocket ships.

Today, we’re more likely to think of innovation in terms of software or services. The heroes of our new age are programmers like Tim Berners-Lee, Sergey Brin, Mark Zuckerberg, and Jack Dorsey—people who stayed up late writing code.

When a coder screwed up, the unhappy results usually played out in the cyber realm. Mistakes could be embarrassing and costly, but they were rarely fatal. The blending of software and hardware raises the risks considerably. If there’s a glitch in the software controlling the probe on the robotic tool your neurosurgeon is using to remove a lesion from your brain, it might create problems that cannot be resolved by upgrading the software in a subsequent release.

“It’s easy to talk about disruption and innovation if you’re writing consumer-facing software, because the risks are relatively low,” says Jeff Erhardt, the CEO of Wise.io, a company that builds machine learning applications for the customer experience market. “But it’s a different story when you’re creating products with longer lifecycles.”

If you’re designing microchips that go into mobile phones, cars, airplanes, and medical devices, the cost of making mistakes can be truly catastrophic. If your chips fail years later, your company can be held financially responsible. There’s also a moral responsibility: When critical hardware components malfunction, people can be injured or killed.

Resistance is Natural: Where There’s a Will, There’s a Way

Erhardt began his technology career at Advanced Micro Devices, where he pioneered the use of large-scale data and advanced analytics for driving new technology development and manufacturing. A serial innovator, he holds more than 30 patents. Still, he isn’t surprised when he encounters institutional resistance to innovation.

“There are valid reasons for resisting innovation, especially when the costs of failure are high. It’s natural to resist change, but it’s also irrational. You have to recognize that it’s a problem and you have to start thinking of practical ways to innovate despite your resistance,” says Erhardt.

Boeing, for example, manages risk and builds highly innovative airplanes, such as the 787 Dreamliner, the first jetliner constructed with significant amounts of lightweight carbon fiber-reinforced plastics and composites to save fuel. Despite a series of highly publicized mishaps in early flights, the fuel-sipping airplane is expected to begin generating profits for Boeing this year.

Even when the situation isn’t potentially life threatening, the challenges of innovating for the real world are more concrete than abstract. For example, when Knock, a small startup in Portland, Oregon, began developing Ride Report, a smartphone app that collects bicycle ridership data, one of the critical challenges it faced was figuring out whether people using the app were driving, walking, or riding bikes.

“People who use the app don’t want to have to tell you whether they’re driving on a highway, walking on a sidewalk, or biking through a park,” says William Henderson, Knock’s founder and CEO. “So we needed a way of determining their mode of transportation quickly and efficiently.”

The easy solution would have been aggressively cranking up the GPS in each user’s phone and collecting more granular data, but that would have drained the phone’s battery faster and probably would have angered users. Knock needed a fast and easy way to determine how people were moving from Point A to Point B.

Here’s where Henderson’s experience as an engineer came in handy. Prior to launching Knock, Henderson had been the lead engineer for Square, which makes those tiny credit card readers that merchants attach to their smartphones. At Knock, he developed an app that enables people to unlock their computers with their iPhones by “knocking” them twice, instead of entering a password.

Clearly, Henderson knows his way around the guts of an iPhone. Newer iPhones are equipped with the ultra-fast A7 processor and a coprocessor called M7 that’s really good at sensing motion without draining the phone’s battery. “Riding a bike generates a distinct repetitive motion pattern that we can recognize using the M7,” he explained. “That made everything a lot easier.”

But that didn’t mean Henderson and his crew had solved every problem. “There’s an aerial tram in Portland with a side-to-side motion that’s very similar to riding a bike,” he says. “You have to keep going back and grinding at the problem until you’ve got a solution that’s good enough.”

Waiting for the Business Model to Gel

In the case of Ride Report, overcoming the technology challenges proved less daunting than finding the right business model. Initially, Knock had to convince the City of Portland that it made economic sense to collect “big data” on bicycle ridership.

The insight generated by Ride Report would enable the city to plan its bikeways more efficiently, based on the actual behavioral patterns of real cyclists. Instead of relying on volunteer surveys, the city could base its decisions on hard facts—and avoid wasting resources on infrastructure that riders didn’t want.

“We could have launched Ride Report years ago, but the business model didn’t really emerge until we began working with the city,” says Henderson. “The business model was the key innovation, not the technology.”

Knock is still working closely with city officials and evolving its business model to provide a portfolio of analytic services that cities will find valuable. “Today, the cities we serve generally see Ride Report as a data pipe,” says Henderson. “Longer term, we’re hoping they’ll use it as an analytics platform that transforms the way they do city planning.”

When in Doubt, Do It Yourself

Henderson’s experience with Ride Report shows the importance of synchronizing technology innovation with business innovation. Even if you create the best and coolest new app, you still need a marketing team to generate demand, and you need a sales team to close the deal with potential customers. If you’re innovating in the hardware space, you’ll need even more.

Ben Einstein is co-founder and managing director of Bolt, a venture capital fund focused on early-stage hardware startups. As an investor and product designer, he’s seen practically every mistake a hardware startup can make. One of the worst mistakes is trying to outsource the design or manufacture of innovative products.

“Young hardware companies want to do that, and it almost never goes well,” says Einstein. “In some businesses, there’s a tradition of outsourcing what you don’t know. We promote the opposite: Learn what you don’t know, or your mistakes will come back to haunt you.”

Let’s say you’re designing a product with a handle. Your first instinct will be to ask your friends and coworkers if the handle is okay. That would be a bad way to test the handle, since your friends and coworkers are less likely to tell you the truth than total strangers. Most people don’t enjoy talking to total strangers, but when you’re developing a new product, you have to do exactly that—assuming you want to find out if the handle works before the product is actually manufactured. “You need to go out and talk to people about your product before you start building it,” says Einstein.

Microprocessors are embedded in many of today’s new hardware products, introducing an entirely new dimension of complexity. Choosing the right microprocessor can make or break a product. “Product developers will pick a microprocessor they have used in the past without really thinking through the consequences,” says Einstein. “Then they find out that each processor now costs $50 and ordering them requires a 50-week lead time. With hardware, your early decisions cast a very long shadow. Sometimes having a 30-minute conversation about a product can avoid months or years of delay.”

Planning for Innovation

Even if you’re not trying to design and build a digital mousetrap from scratch in a country 6,000 miles away, you will still find innovation challenging.

Thanks largely to Christensen’s pioneering insight, almost every large company has developed some kind of program or process to smooth the path for innovation. Many of them, however, lack rigorous or repeatable processes.

The Clorox Company is among a handful of notable exceptions. Clorox has two programs, !nnovent and the Creative Coalition, operating within its Open Innovation Strategy.

!nnovent is basically an ongoing internal competition run by the company’s R&D department. All Clorox employees are encouraged to submit ideas for new products or business processes. The program has three rounds:

- Round 1: Dream !t (five weeks): Employees post their ideas for growth; all employees vote and the top 30+ ideas move on to the next round.

- Round 2: Drive !t (three weeks): The top ideas from Round 1 are built into business cases. A business panel votes and the top eight ideas move to the final round.

- Round 3: Do !t (three months): Teams are formed around the top eight ideas. The Teams are given time (10% of work hours), funding ($3,000), specialized training, and access to mentors. The teams write business plans and pitch the plans to the Executive Committee, which includes the CEO. The committee picks an idea (or ideas) to put into production.

Clorox’s Creative Coalition is managed by the company’s Global Insight group. The coalition is made up of “thought partners” chosen from various fields and screened for their creativity, teamwork, and ability to articulate new ideas. They receive special training in ideation and function as an “on-demand” source of fresh innovation.

For Clorox, the effort to create substantive innovation processes has paid off. In each of the past five fiscal years, new products have generated about 3 percentage points of annual incremental sales growth for the company. That growth represents significant gains for the company’s top line, as well as increased market share for Clorox products.

Revolution, Innovation and Disruption

It’s hard to write about innovation without mentioning Christensen’s extremely useful books on the topic, including The Innovator’s Dilemma (HarperBusiness) and The Innovator’s Solution (Harvard Business Review Press), which he co-authored with Michael Raynor. Another staple in the innovation genre is The Lean Startup by Eric Ries (Viking). With those three books under your belt, you can join just about any conversation about innovation and appear reasonably knowledgeable on the subject.

A book that’s often overlooked in discussions about innovation is The Structure of Scientific Revolutions by Thomas Kuhn (University Of Chicago Press). In addition to thrusting the term “paradigm shift” into the popular lexicon, Kuhn’s book serves as a vivid reminder that innovation is almost always messy—and occasionally bloody. Kuhn’s analysis suggests that moments of genuine innovation are like earthquakes: huge amounts of energy, released over a relatively brief period of time, disrupt and transform the surrounding landscape.

Because innovation is inherently disruptive, it always poses challenges to the status quo. Nobody really likes change; we’d all prefer sticking to our routines. That’s why terms like “creative destruction” tend to irritate us. We all support creativity, but we’re not thrilled by destruction, unless it’s part of a video game or disaster movie.

Greg Fell, a venture capitalist and former chief information officer, says he switched his college major from computer science to philosophy after reading Kuhn’s book. “It’s a template for understanding the progress of science and technology,” says Fell, who built a successful career in corporate IT by carefully blending technology and business innovation.

For early stage investors, understanding the rhythm and flow of innovation is absolutely critical. Contrary to popular belief, even the shrewdest investors hedge their bets, because you can never be certain if an exciting new idea is genuinely innovative, or just plain crazy. “If you’re a venture capitalist and you can hit one out of ten, you’ll get a nice return on the money you invest,” says Fell. “If you can hit two out of ten, you’ll become a billionaire.”

It seems odd that VCs are held to even lower standards of success than professional baseball players. In major league baseball, the mythical “Mendoza Line” (a .200 batting average) is considered the minimum performance standard for all players except pitchers. When you consider that Ted Williams’ career average was “only” .344, that leaves plenty of room for failure.

Inspiration, Perspiration, and Battling the Status Quo

Even at its best, technology innovation tends to be lumpy and uneven, with plenty of downtime in between “Eureka” moments.

“Scientific revolutions or ‘paradigm shifts’ are followed by periods of ‘puzzle solving’ in which scientists and researchers work within the new paradigm to strengthen or refine its basic principles,” says Fell. “When you’re between paradigm shifts, you’re not striving for creativity or originality. You’re focused on incremental refinements.”

From a business perspective, refinements mean concentrating on achieving greater efficiencies and lower costs, optimizing processes or improving existing products. Typically, those kinds of activities are highly rewarded, since they can easily make a company’s bottom line look better in the short term.

Growing the top line requires a different approach and a longer timeline. There’s an old saying that you cannot save your way to greatness. The only way to grow the top line is by selling products or offering services your competitors cannot easily duplicate at lower prices. Staying ahead of the competition requires constant and relentless innovation. Both Kuhn’s and Christensen’s books make it abundantly clear, however, that innovating is not a sport for the timid.

This Too Shall Pass

When I was in college, I sometimes drove to visit friends in Boston. Driving along Route 128, I marveled at the corporate headquarters of companies like Wang Laboratories, Data General, Prime Computer, Apollo Computer, and the Digital Electronics Corporation. I desperately wanted to work at one of those fabled companies and I assumed they would remain there forever as living monuments to the power of science.

None of those companies exist today. Each was disrupted out of existence by sharper, faster, bigger, or more agile rivals. Disruptive innovation isn’t one of those “black swan” events described by Nassim Nicholas Taleb. It’s a common occurrence, a fact of life. William Ruh, the newly-appointed chief digital officer at GE, recently told an audience that any company can be disrupted at any time. Innovation is the only defense, and the only long-term strategy for survival.