Chapter 5

Main financial statements: The statement of financial position (balance sheet)

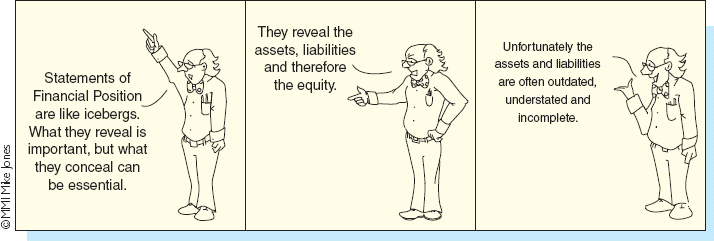

‘Creative accounting practices gave rise to the quip, “A balance sheet is very much like a bikini bathing suit. What it reveals is interesting, what it conceals is vital.”’

Abraham Briloff, Unaccountable Accounting, Harper & Row (1972). The Wiley Book of Business Quotations (1998), p. 351

Learning Outcomes

After completing this chapter you should be able to:

- Explain the nature of a statement of financial position.

- Understand the individual components of a statement of financial position.

- Outline the layout of a statement of financial position.

- Evaluate the usefulness of a statement of financial position.

Go online to discover the extra features for this chapter at www.wiley.com/college/jones

Go online to discover the extra features for this chapter at www.wiley.com/college/jones

Chapter Summary

- One of three main financial statements.

- Consists of assets, liabilities and equity.

- Assets are most often non-current (e.g., property, plant and equipment such as land and buildings, plant and machinery, motor vehicles, and fixtures and fittings) or current (e.g., inventory, trade receivables, cash).

- Liabilities can be current (e.g., trade payables, short-term loans) or non-current (e.g., long-term loans).

- Listed companies have a special terminology and presentational format for ...

Get Accounting, 3rd Edition now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.