July 2011

Intermediate to advanced

741 pages

17h 32m

English

COMPLETE SOLUTION TO THE ILLUSTRATION

T-1 On introducing cash into the fund:

T-2 On purchase of Bonds—FVPL:

T-3 On recording accrued interest purchased on purchase of Bond:

T-4 On payment of contracted sum:

T-5 On accounting for interest on coupon date:

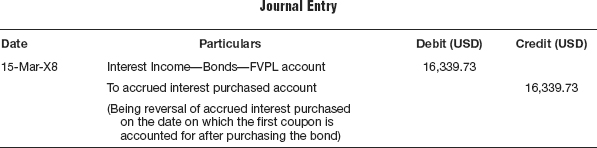

T-6 On reversal of accrued interest purchased:

T-7 On receipt of coupon interest in the bank:

T-8 On accounting for interest based on amortization:

T-9 On valuation of bond at the end of valuation date:

The market value is given in the example, $86.50 per bond as on 31-Mar-X8. The amortized cost as on date is arrived at with the carrying cost end price per bond on 31-Mar-X8 and the numbers of bonds held. Thus, in the example as on 31-Mar-X8, ...

Read now

Unlock full access