CHAPTERSEVEN

Single Risk Closed-Form Approximations of Asymptotic Tail Behaviour

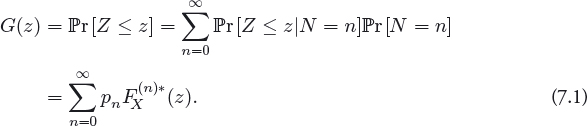

In Chapter 6, a set of special sub-families of annual loss loss distribution approach (LDA) models were developed which admitted closed-form exact representations. That is, closed-form representations were obtained for the distribution of the annual loss Z = X1 + · · · + XN represented by a compound process model with LDA structure in which the frequency is N ~ Poisson(λ) and the severities are independent and identically distributed (i.i.d.) Xi(t) ~ FX(x), and N and Xi are independent. The exact distribution of the annual loss processes can be expressed analytically as a mixture distribution comprised convolved distributional components with Poisson mixing weights for N > 0,

Here, ![]() =

= ![]() r[X1 + X2 + · · · + Xn ≤ z] is the n-th convolution of the severity distribution FX(·) calculated recursively as

r[X1 + X2 + · · · + Xn ≤ z] is the n-th convolution of the severity distribution FX(·) calculated recursively as

![]()

with ![]() = 1 if z ≥ 0 and zero otherwise. Note, throughout this chapter we refer to F as the distribution for the severity, ...

= 1 if z ≥ 0 and zero otherwise. Note, throughout this chapter we refer to F as the distribution for the severity, ...

Get Advances in Heavy Tailed Risk Modeling: A Handbook of Operational Risk now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.