Chapter 28

MEASURING VALUE CREATION

Separating the wheat from the chaff

Creating value has become such an important issue in finance that a host of indicators have been developed to measure it. They come under a confusing array of acronyms – TSR, MVA, EVA, CFROI, ROCE-WACC – but most of these will probably be winnowed out in the years to come. Ultimately, they should be reduced to those few that best mirror and address the recent developments in cash flow statements.

The current profusion of indicators has its advantages, as normally we expect only the most reliable to survive. However, in practice some companies use the lack of clear guidelines and standards to choose indicators that best serve their interests at a given time, even if this involves the laborious task of changing indicators on a routine basis.

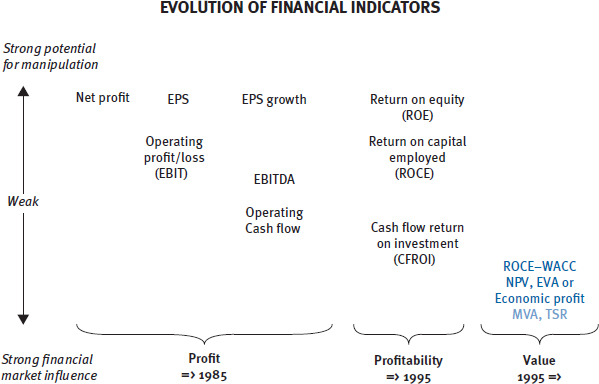

The chart below should help you find your way through the maze of indicators. It plots the chronological appearance of value measures according to three criteria: ease of manipulation, sensitivity to financial markets and category (accounting, economic or stock market indicators).

Accounting, financial, hybrid and stock market criteria

Section 28.1

OVERVIEW OF THE DIFFERENT CRITERIA

Predictably, the indicators cluster around a diagonal running from the upper left-hand corner down to the lower-right hand: this reflects companies' diminished ability to manipulate the indicators ...

Get Corporate Finance Theory and Practice, Third Edition now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.