CHAPTER 6

Register Disbursement Schemes

OVERVIEW

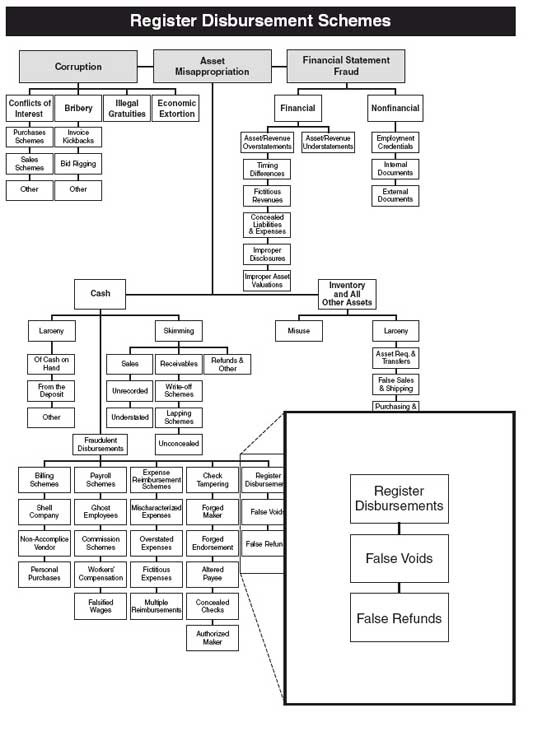

So far we have discussed two ways in which fraud is committed at the cash register: skimming and cash larceny. These schemes are what we commonly think of as theft. They involve the surreptitious removal of money from a cash register. When money is taken from a register in a skimming or larceny scheme, there is no record of the transaction—the money is simply missing.

In this chapter, we discuss fraudulent disbursements at the cash register. These schemes differ from the other register frauds in that when money is taken from the register, the removal of money is recorded on the register tape. A false transaction is recorded as if it were a legitimate disbursement to justify the removal of money. Bob Walker's fraudulent refunds in the next case study were an example of such a false transaction.

Two basic fraudulent disbursement schemes take place at the register: false refunds and false voids. Although the schemes are largely similar, there are a few differences between the two that merit discussing them separately.

Get Corporate Fraud Handbook: Prevention and Detection, 4th Edition now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.