Chapter 2

The Creative Accounting and Fraud Environment

2.1 INTRODUCTION

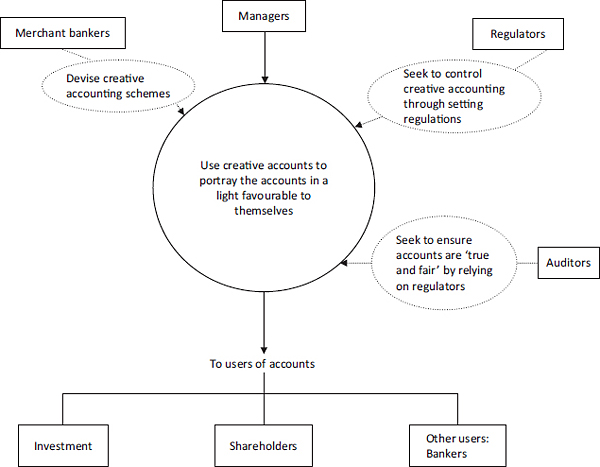

Creative accounting and fraud do not occur in a vacuum. There are a number of interested parties. These range from managers, investment analysts, auditors, regulators, shareholders, merchant bankers to other users. As can be seen from Figure 2.1, all of these parties play a key role in creative accounting. In the case of fraud, the legal authorities will also take an interest. The corporate environment of the firm and economic climate are also important. There needs to be, in particular, effective corporate governance. For instance, Crutchley, Jensen and Marshall (2007, p. 53) comment: ‘[W]e find that the corporate environment most likely to lead to an accounting scandal is characterised by rapid growth, with high earnings smoothing, fewer outsiders on the audit committee, and outsider directors that seemed overcommitted.’ Finally, the economic environment of the company, or the personal circumstances of an individual, are important. Creative accounting and fraud are more likely when a company is facing financial difficulties.

Figure 2.1 The parties to creative accounting

The managers set the creative accounting agenda. They wish to portray the accounts in a light favourable to themselves. This may be to increase profits or increase net assets. The flexibility in accounting allows them to select ...