CHAPTER 3Problems with Legislation and Those Involved in the Financial Information

A balance sheet is inevitably false, because either things are valued for what they have cost, and what they have cost is not generally what they're worth, or we pretend to write them down for what they're worth and, how can we know the value of something we don't know when and at what price we will sell?

—Auguste Detoeuf (1883–1947), founder of Alsthom

3.1 HOW FINANCIAL INFORMATION IS GENERATED

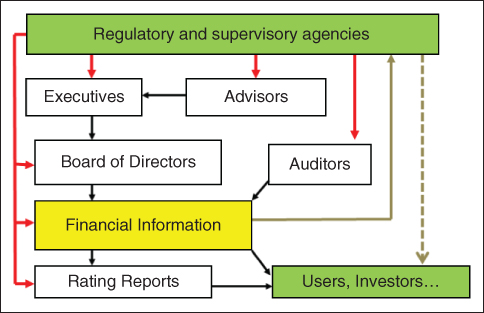

When companies' financial information reaches users (mainly shareholders, credit institutions, and creditors), it has followed a process as the one shown in Figure 3.1. The company's executives prepare the accounts, the board of directors formulates them and the annual general meeting approves them. Auditors also intervene to express their opinion on the reasonableness of the accounts in accordance with current accounting and auditing standards. Finally, the analysts and rating companies that assess and comment on the situation and perspectives of the company also participate. The quality of this process is followed by supervisory agencies.

FIGURE 3.1 Agents that intervene in the formulation, approval, control, and diffusion of the financial information

In regard to the company's executives and the board of directors, there are factors that can condition negatively. The pressure to obtain the expected ...

Get Detecting Accounting Fraud Before It's Too Late now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.