CHAPTER 4Why Are Accounts Manipulated?

Fraud is the daughter of greed.

—Jonathan Gash

4.1 MOTIVATION, OPPORTUNITY, AND RATIONALIZATION

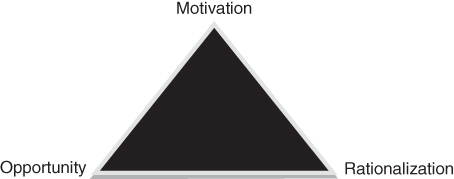

Those who manipulate accounts do it for multiple reasons, but to understand the process that leads to the existence of these frauds is illustrative the so-called Triangle of Fraud (Cressey 1980). This is a model (see Figure 4.1) that explains the three factors that, when they coincide in time, lead to the commission of fraud. The criminologist Donald Cressey formulated his triangle theory after interviewing over 300 prisoners jailed for having committed several offenses. From the interviews' results, he identified the circumstances that coincide in most offenses.

FIGURE 4.1 The Triangle of Fraud (Cressey, 1980)

- Motivation: The need or pressure that encourages interest in defrauding. Some examples of motivations that exert pressure to defraud are:

- Sales and profit decrease and there is an interest in hiding this decline from bankers or shareholders.

- Paying fewer taxes.

- A company that will be sold, or will start listing in the stock market, and wants to offer better figures.

- A company that has to make an employment regulation or has to ask for subsidies and wants to offer worse figures.

- A manager who wants the profits to be higher to receive a higher variable compensation.

- Opportunity: A situation that allows defrauding with a low risk ...

Get Detecting Accounting Fraud Before It's Too Late now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.