(5.46)

(5.46)

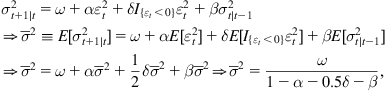

where ![]() holds for all symmetric distributions with zero mean, for which the magnitude of

holds for all symmetric distributions with zero mean, for which the magnitude of ![]() and therefore of its square does not depend on the sign of

and therefore of its square does not depend on the sign of ![]() and

and

(5.47)

More ...

Get Essentials of Time Series for Financial Applications now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.