Chapter 1FORECASTING PREREQUISITES

LEARNING OBJECTIVES

The purpose of the first chapter is to acquaint you with some basic ideas about forecasting. After completing this chapter, you should be able to do the following:

• Identify the basic forecasting process.

• Distinguish the differences between budgets and forecasts.

• Identify how growth can affect a company

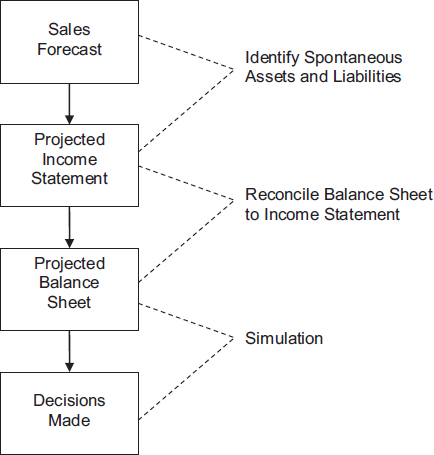

An Overview of the Forecasting Process

Forecasting involves looking into the future, but we base it in part on financial relationships from the past and upon expectations about the future. The model that we are using today is a sales-driven model. The most basic underlying assumption is that the firm, its size, and its financial condition are very closely tied to sales.

This model presumes some ability to forecast sales. For a company that cannot forecast where its sales are headed, this model may not be appropriate. This statement does not mean that you need a 100- percent-accurate sales forecast. In fact, all you need is a sales direction and a reasonable approximation of the magnitude of the sales change. A range of possible sales figures can be used in place of a single number. From the sales forecast the analyst then relates the various balance sheet accounts and expenses to the anticipated sales change. Finding these relationships allows the analyst to complete pro forma financial statements and ...

Get Financial Forecasting and Decision Making now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.