January 2014

Intermediate to advanced

454 pages

11h 8m

English

In the classical linear regression model, the multivariate regression hyperplane has the form

where we have m predetermined explanatory variables or regressors X1, ..., Xm and ε is a random error term. Here Equation 6.1 depicts a linear regression model since it is linear in the parameters β0, β1, ..., βm. It is assumed that n > p = m + 1 and no exact linear relationship exists between the Xj's, j = 1,..., m.

For fixed Xj's, j = 1,..., m, the population regression hyperplane is specified as the conditional mean of Y given the Xj's or

given that E(ε) = 0. Given Equation 6.2,

![]()

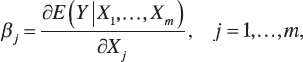

that is, the population intercept is the mean of Y given that all of the Xj's are set equal to zero. Also,

is termed the jth partial regression coefficient; that is, as Xj increases by one unit, the average value of Y changes by βj units, given that all remaining explanatory variables are held constant. Once the βk's, k = 0, 1,..., m, are estimated from the sample information, we obtain the sample regression hyperplane

where Ŷ is the estimated value of ...

Read now

Unlock full access