CHAPTER THIRTY-THREE

Activity-Based Budgeting

INTRODUCTION

The purposes of this chapter are to discuss problems with traditional budgeting, define activity-based budgeting (ABB), and discuss the ABB process.

A budget is a financial expression of a plan. Traditional budgeting focuses on planning resources for an organizational unit. Each year managers look at history and any significant changes and create an annual budget. The budgeting process starts with the senior executive’s announcing budget goals. These may consist of revenue and profit goals as well as goals for new services.

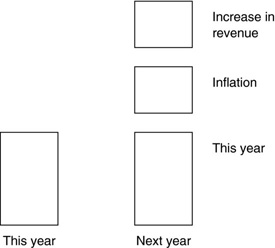

Many managers respond by looking at last year’s numbers and increasing their budget for the year based on inflation and/or the amount of the increase in revenues (see Exhibit 33.1). For example, if revenues increase 10 percent, then the various department managers might increase the budgets for their departments by 10 percent.

Exhibit 33.1 Manager’s Response to Next Year’s Forecast

The problem with this approach is that last year’s inefficiencies are incorporated into this year’s budget. Often little attention is paid to improvements in each department. Finally, little incentive is incorporated into the budgeting process for continuous improvement. Changing workload for each department ...