CHAPTER 12

INCOME TAX EXPENSE AND ITS LIABILITY

Taxation of Business Profit

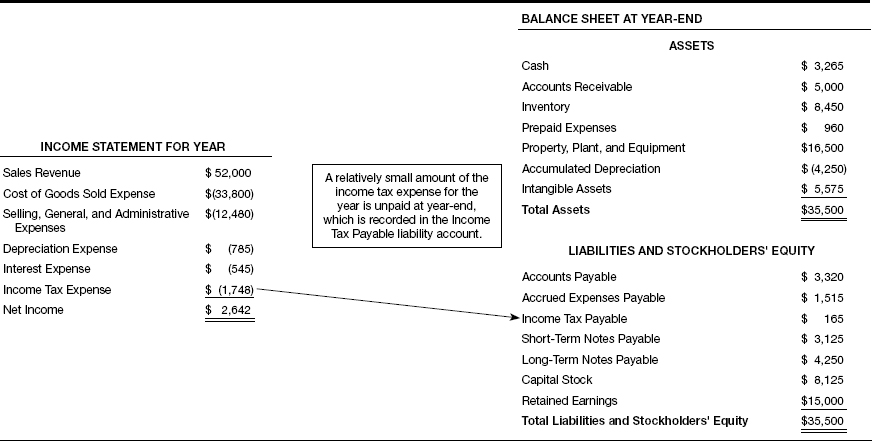

Please refer to Exhibit 12.1 at the start of the chapter, which highlights the connection between income tax expense in the income statement and the income tax payable liability in the balance sheet. Chapter 3 explains the accounting entry for recording income tax expense. Income tax expense is increased and the income tax liability is increased. The liability account is decreased as cash payments are made (and cash is decreased). Typically, not all of the income tax expense for the year is paid by the end of the year. In this company example a small part of the company’s total income tax expense for the year, which is based on its taxable income for the year, has not been paid at year-end. This remaining balance will be paid in the near future. The unpaid portion stays in the company’s income tax payable liability account until paid.

EXHIBIT 12.1—INCOME TAX EXPENSE AND INCOME TAX PAYABLE

Dollar Amounts in Thousands

The business in our example is incorporated; the business decided on this form of legal organization (instead of a partnership or limited liability company). A corporation, being a separate person in the eyes of the law, has several important advantages. However, profit-motivated business corporations have one serious disadvantage—they are subject to federal and state income tax on their profits, ...

Get How to Read a Financial Report: Wringing Vital Signs Out of the Numbers, 8th Edition now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.