CHAPTER 17

FOOTNOTES TO FINANCIAL STATEMENTS

This is the first of three chapters that discuss analyzing the information in business financial reports. This and the next chapter consider the information in external financial reports—those that circulate outside the business. These financial communications are designed mainly for the outside shareowners and lenders of the business, who are the two primary stakeholders in the business. The managers of a business have access to more information than released in the company’s external financial reports. Chapter 19 discusses how managers can use the inside information for analyzing profit performance.

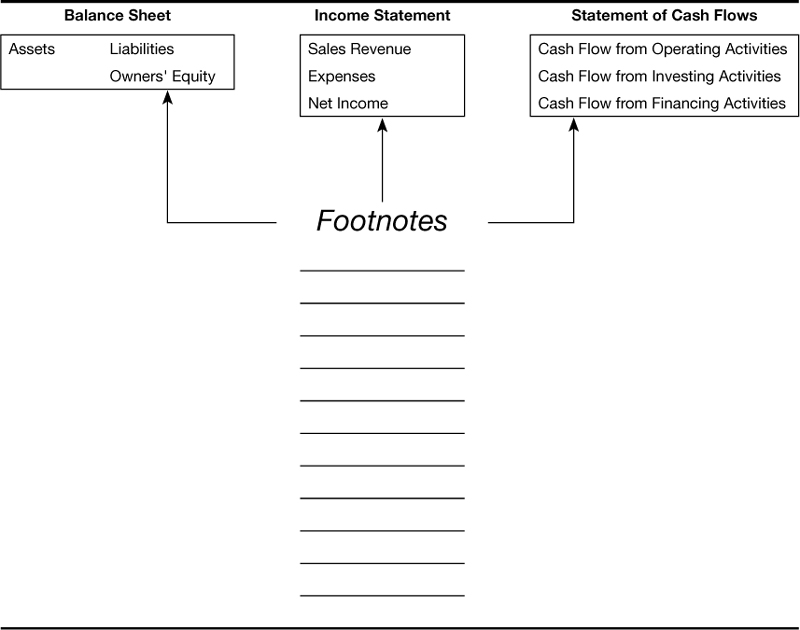

Exhibit 17.1 at the start of the chapter summarizes the principal elements of the three financial statements of a business and shows that footnotes are included with the three statements. Footnotes are the fourth essential part of every financial report. Financial statements would be “naked” without their footnotes. This chapter explains the importance of reading the footnotes and problems with footnotes. Studying a financial report should definitely include reading the footnotes to the financial statements.

EXHIBIT 17.1—THREE FINANCIAL STATEMENTS AND FOOTNOTES

Financial Statements—Brief Review

Before discussing footnotes, let’s quickly review the three financial statements of a business that we explain in previous chapters.

Get How to Read a Financial Report: Wringing Vital Signs Out of the Numbers, 8th Edition now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.