October 2012

Beginner

420 pages

9h 37m

English

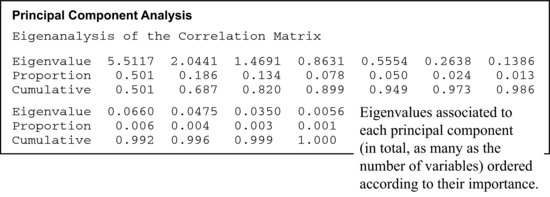

24.2 Principal Components

Statistical method used to compute new variables function of the original ones. These new variables are called ‘principal components’ and it is expected that few of them contain most of the information in the data.

Stat > Multivariate > Principal Components

The first part on the shown output list provides information on the magnitude of the eigenvalues, ordered from highest to lowest, on the proportion they represent with respect to the total (proportion of the global variability explained by this component), and on the cumulative proportion.

Read now

Unlock full access