CHAPTER 11A Few Use Cases

We conclude the Data Operations part of the book by illustrating some common time series operations in kdb+/q and a demo of a real-time CEP engine.

11.1 ROLLING VWAP

The first example originates in high-frequency finance. Any update in the market will result in an update (tick) in our data. It is of fundamental importance for any market participant to understand the current state of the market. For this purpose, various statistics and indicators are needed to monitor market activity. Let us assume that we wish to calculate a moving VWAP (Volume Weighted Average Price) over a rolling window. We will cover two use cases.

11.1.1 N Tick VWAP

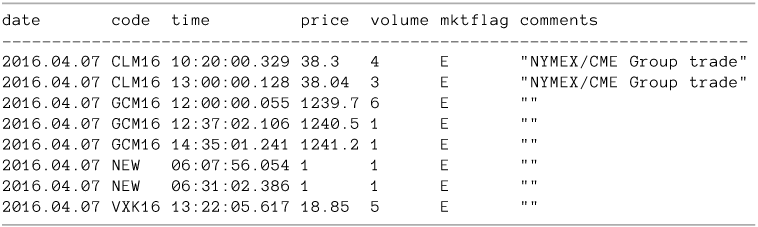

Here, we can make use of the msum function we saw in Chapter 3 to calculate the moving VWAP for, say, 2 consecutive ticks. Using our standard trades table trd from our hdb mydb:

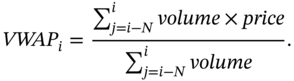

and the definition of a ![]() -tick VWAP at tick

-tick VWAP at tick i

The 2-tick vwap for each symbol is

11.1.2 Time Window VWAP

For a moving time-window ...

Get Machine Learning and Big Data with kdb+/q now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.