March 2019

Intermediate to advanced

680 pages

13h 56m

English

Similar to principle component analysis, factor analysis is one of the commonly used dimension reduction methods. It is a statistical technique widely used to explain a m‐dimensional vector with a few underlying factors. After introducing different methods to derive factors, we will illustrate the method with empirical examples. We will also discuss its use in forecasting.

Just like principle component analysis, the purpose of factor analysis is to approximate the covariance relationships among a set of variables. Specifically, it is used to describe the covariance relationships for many variables in terms of a relatively few underlying factors, which are unobservable random quantities. The concept was developed by the researchers in the field of psychometrics in the early twentieth century. It has become a commonly used statistical method in many areas.

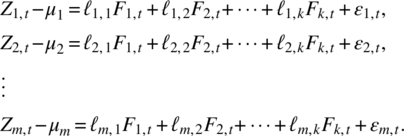

Given a weakly stationary m‐dimensional random vector at time t, Zt = [Z1,t, Z2,t, …, Zm,t]′ with mean μ = (μ1, μ2, …, μm)′, and covariance matrix Γ, the factor model assumes that Zt is dependent on a small number of k unobservable factors, Fj,t, j = 1, 2, …, k, known as common factors, and m additional noises εi,t, i = 1, 2, …, m, also known as specific factors, that is

More compactly, we can write the system in following ...

Read now

Unlock full access