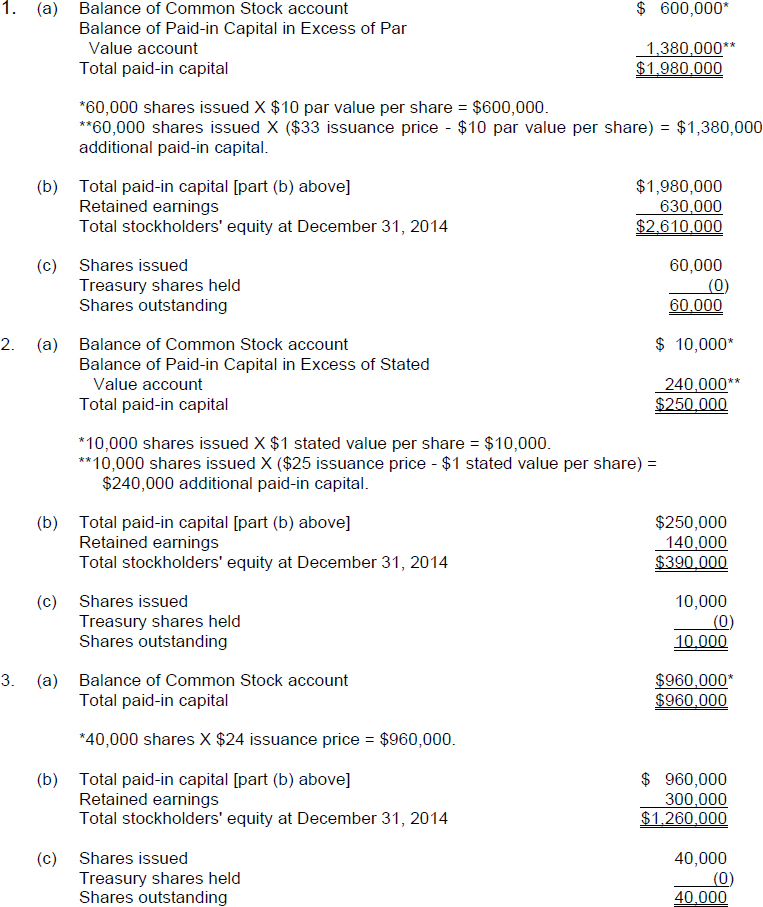

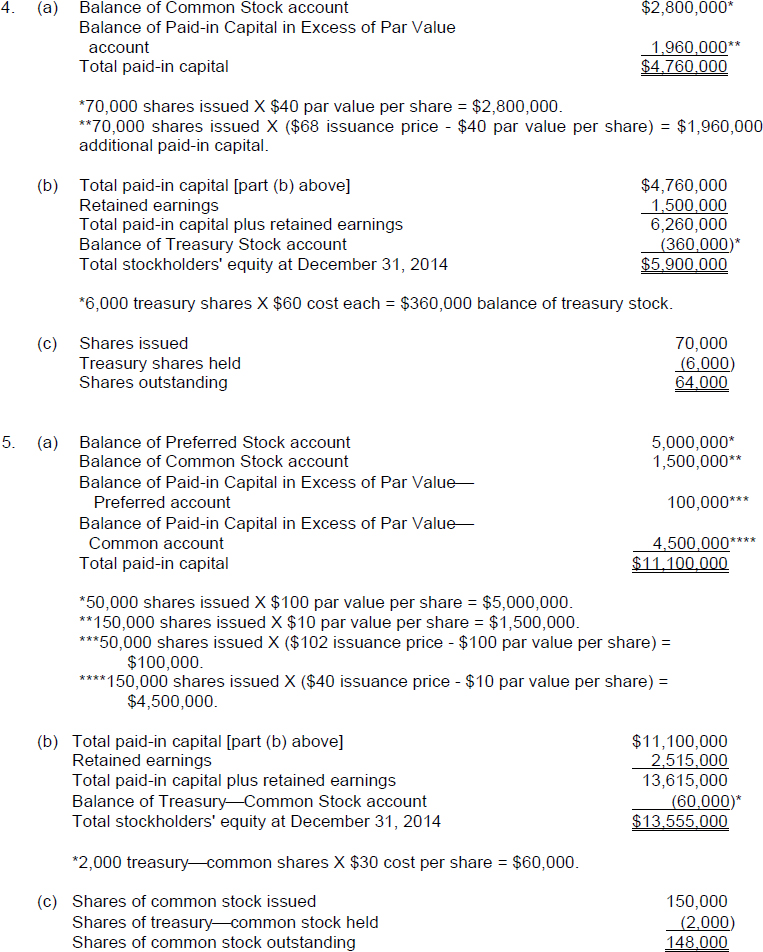

SOLUTION TO EXERCISE 11-2

Explanation:

(a) Total paid-in capital is determined by the sum of the balances of the capital stock account(s) and any additional paid-in capital accounts (such as Paid-in Capital in Excess of Par or Stated Value and Paid-in Capital from Treasury Stock). When a par value stock (or a no-par stock with a stated value) is issued at a price above par (stated value), the par value (stated value) is recorded in the appropriate capital stock account (Common Stock or Preferred Stock) and the excess of issuance price over par (stated) value is recorded in an additional paid-in capital account (Paid-in Capital in Excess of Par [Stated] Value).

(b) Total stockholders' equity is the sum of the balances of the paid-in capital accounts and the Retained Earnings account less the balance of the Treasury Stock account.

(c) The number of common stock shares outstanding is the number of common stock shares in the hands of shareholders; it is determined by deducting the number of treasury common stock shares from the number of issued common shares.

Get Problem Solving Survival Guide to accompany Financial Accounting, 8th Edition now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.