SOLUTION TO EXERCISE 2-5

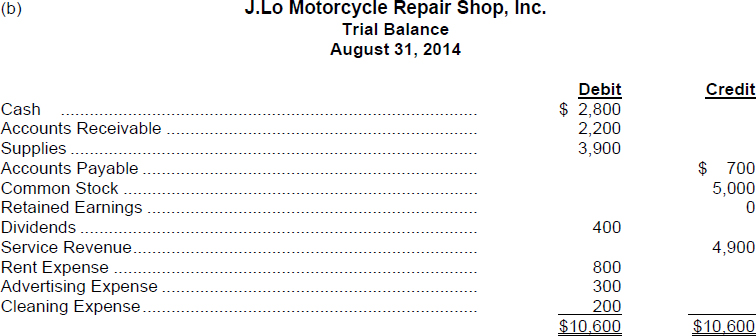

(c) A trial balance is a list of the accounts and their balances at a given point in time. A trial balance serves several purposes, including:

- It proves that the ledger is in balance (that is, that total debits equal total credits in the ledger accounts). If errors are made in journalizing and posting, they may be detected in the process of preparing a trial balance.

- It is a starting point for organizing the information to be reported on a company's financial statements.

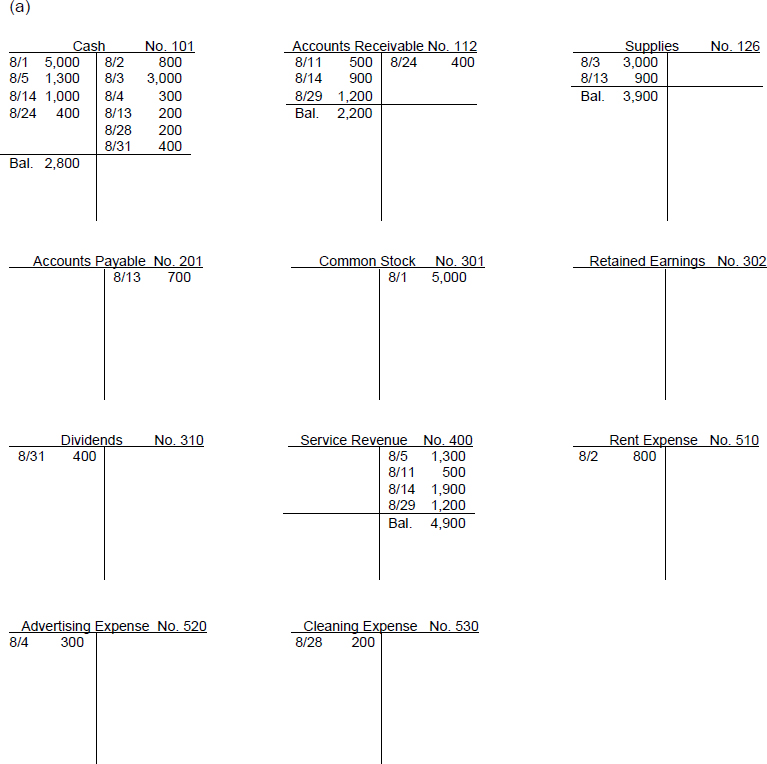

TIP: Scan over Exercises 2-3, 2-4, and 2-5. Notice the logical progression of the steps in recording, classifying, and summarizing the transactions. In Exercise 2-3, each transaction had to be identified and analyzed in terms of its effects on various accounts. Then the transactions were recorded in the journal. In Exercise 2-4, the information in the journal is transferred (posted) to the ledger. Thus, all transactions that affect individual components of the basic accounting equation are summarized together. In Exercise 2-5, the accounts are balanced, and a trial balance is prepared which furthers the summarization process and checks for the maintenance of equality of debits and credits in the recording and posting phases.

Get Problem Solving Survival Guide to accompany Financial Accounting, 8th Edition now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.