EXERCISE 5-4

| Purpose: | (L.O. 1, 2, 3, 5, and 6) This exercise reviews the elements of the net sales, cost of goods sold, gross profit, total operating expenses, and net income computations for a merchandising company. |

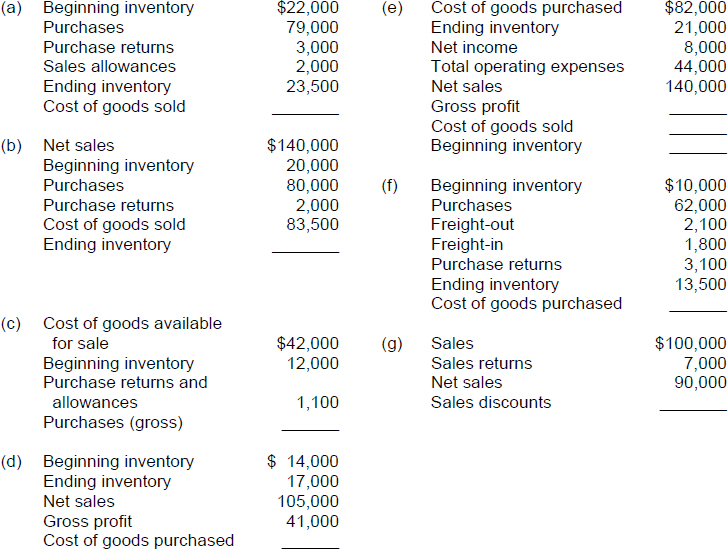

Instructions

Compute the missing amounts for each of the independent situations below.

TIP: Be careful to distinguish between purchase allowances and sales allowances. Sales allowances are reductions in sales prices allowed to customers. Purchase allowances are reductions in the purchase prices of merchandise from suppliers. Sales allowances are a contra revenue item; purchase allowances reduce the balance of the Inventory account (when the perpetual system is used to record inventory purchases). Likewise, be careful to distinguish between (a) sales returns and purchase returns, and (b) sales discounts and purchase discounts. Returns and discounts processed for customers are related to sales; returns and discounts honored by suppliers of merchandise inventory are related to purchases.

Get Problem Solving Survival Guide to accompany Financial Accounting, 8th Edition now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.