- 14. Generalised Itō Integral. Let

be a probability space and let

be a probability space and let  be a standard Wiener process. Given that

be a standard Wiener process. Given that  is a simple process, show

is a simple process, show

and

Solution

For the first result, using Taylor's theorem on

and subsequently applying Itō's formula we have

and subsequently applying Itō's formula we have

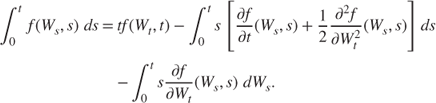

Taking integrals from

to

to  ,

,

and rearranging the terms, finally

since .

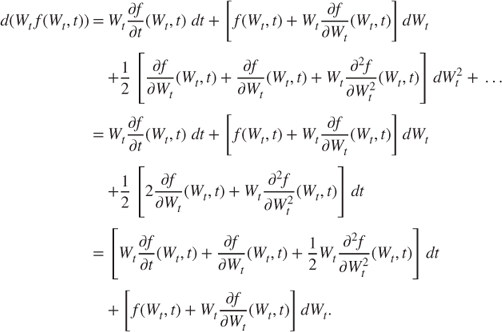

As for the second result, from Taylor's theorem and Itō's formula

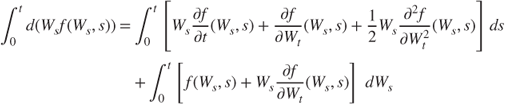

Taking integrals ...

Get Problems and Solutions in Mathematical Finance: Stochastic Calculus, Volume I now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.