(5.20)

(5.20)

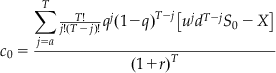

or:

or, in shorthand form:12

where q′=qu/(1+r) and 1−q′=d(1−q)/(1+r). The values q′, q, and T are the parameters for the two binomial distributions. Three points are worth further discussion regarding this simplified binomial model:

1. First, as T approaches infinity, the binomial distribution will approach the normal distribution, ...

Get Risk Neutral Pricing and Financial Mathematics: A Primer now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.