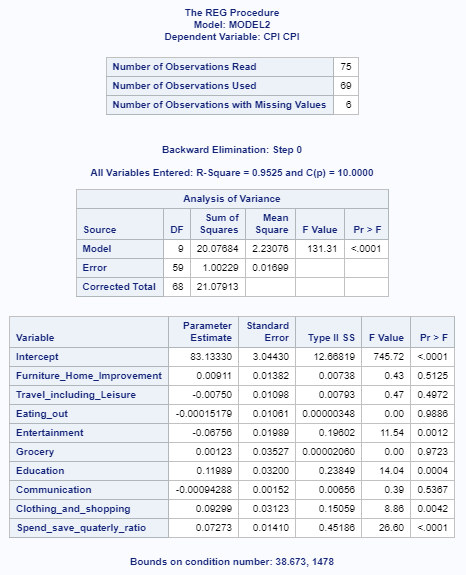

In the backward selection model, our step 0, as shown in the following diagram, includes all the variables that have been included as independent variables. We have calculated the parameter estimates, the F values, and tested for statistical significance of the variable:

Figure 5.16: Backward selection: step 0

The Eating_out variable has the highest p-value in the Figure 5.17 statistics for removal section. In the next section of the output, the Eating_out variable is dropped from the model. New parameter estimates, F values, and test of significance values are generated for the model, as shown in the following diagram: ...