CHAPTER 15

Execution

Execution involves implementing the investment program efficiently. Doing this may involve developing investment manager guidelines and implementing changes across and within asset classes (rebalancing and transitioning between managers). This chapter deals with rebalancing and transitioning assets between managers.

REBALANCING

“Rebalancing” means periodically adjusting a portfolio's asset allocation back to its benchmark, or strategic, asset allocation.

Why Is Rebalancing Necessary?

The fund's strategic asset allocation represents the portfolio that the governing body determines best meets the objectives of the fund, given the risk–return trade-off. The strategic asset allocation is often referred to as the fund's benchmark asset allocation.

Over time, however, the returns to each asset class will differ, and, even if the fund's asset allocation was initially exactly at benchmark, the actual asset allocation will drift away from the benchmark.

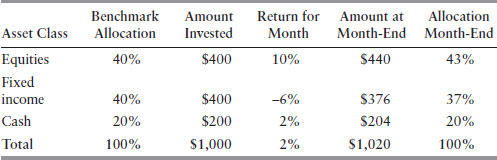

For example, suppose that the benchmark was 40 percent equities, 40 percent fixed interest, and 20 percent cash and that we invested $1,000 in this benchmark asset allocation at the start of the month. Performance during the month is as shown in Table 15.1.

Table 15.1 Example of Portfolio Drift

During the month, each asset class performed differently. Equities returned 10 percent, fixed income fell by 6 percent, and ...

Get Strategic Risk Management: A Practical Guide to Portfolio Risk Management now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.