June 2007

Beginner to intermediate

950 pages

27h 8m

English

This uses the rlm function from the MASS library. The function allows one to fit a linear model by robust regression using an M estimator, allowing robust inference for parameters and robust model selection. The robust fit is minimally influenced by outliers in the response variable, in the explanatory variable(s) or in both.

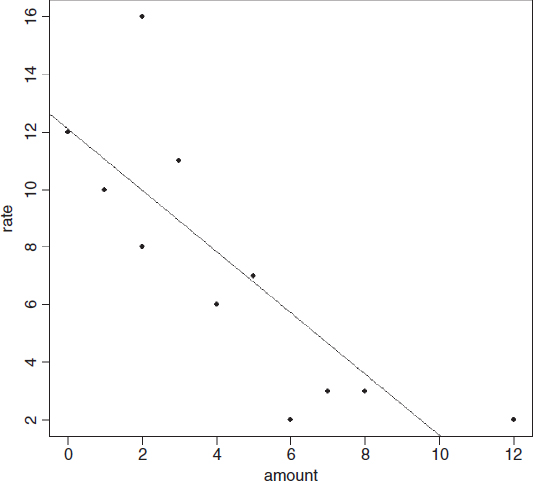

robreg<-read.table("c:\\temp\\robreg.txt",header=T) attach(robreg) names(robreg) [1] "amount" "rate" plot(amount,rate,pch=16) abline(lm(rate~amount)) summary(lm(rate~amount)) Coefficients: Estimate Std. Error t value Pr(>|t|) (Intercept) 12.1064 1.4439 8.385 1.52e-05 *** amount -1.0634 0.2552 -4.166 0.00243 ** Residual standard error: 2.851 on 9 degrees of freedom Multiple R-Squared: 0.6585, Adjusted R-squared: 0.6206 F-statistic: 17.36 on 1 and 9 DF, p-value: 0.002425

We can leave out the maximum and minimum values of the response or explanatory variables separately or together using subset to test for influence:

summary(lm(rate~amount,subset=(rate<max(rate))))

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 10.8163 1.0682 10.126 7.73e-06 ***

amount -0.9201 0.1811 -5.081 0.000952 ***

Residual standard error: 1.964 on 8 degrees of freedom

Multiple R-Squared: 0.7634, Adjusted R-squared: 0.7339

F-statistic: 25.82 on 1 and 8 DF, p-value: 0.000952

The intercept is lower by more than 1.0 and the slope is shallower ...

Read now

Unlock full access