32Divestitures1

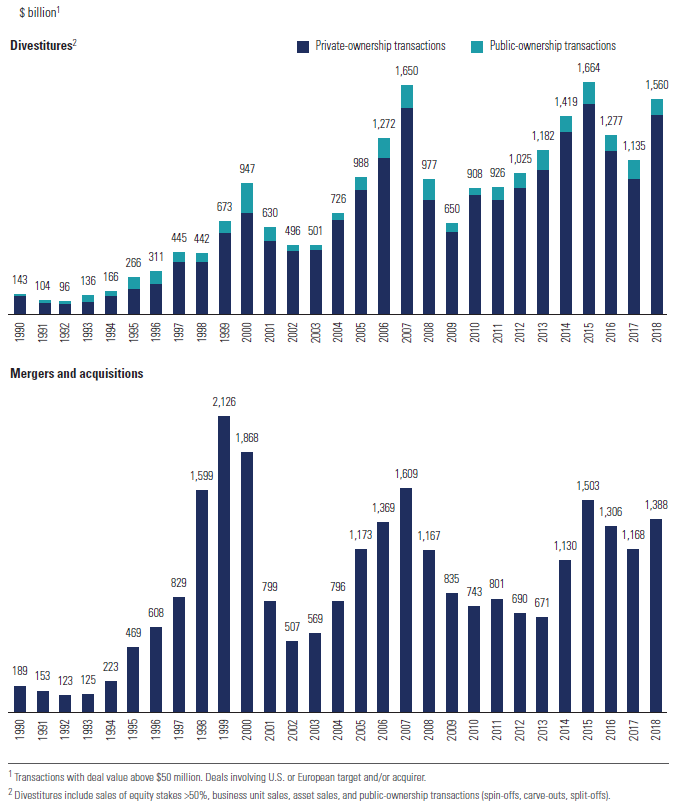

Divestitures, like mergers and acquisitions, tend to occur in waves, as Exhibit 32.1 shows. In the decade following the conglomerate excesses of the 1960s and 1970s, many companies refocused their portfolios. These divestitures were generally sales to other companies or private buyout firms. By the 1990s, divestiture activity included more public-ownership transactions—spin-offs, carve-outs, and tracking stocks. Such public-ownership transactions have since become an established divestment approach, although most divestitures still take the form of deals between companies.

Exhibit 32.1 Divestitures Volume vs. M&A Volume

Source: Securities Data Company; Dealogic; Corporate Performance Analysis by McKinsey.

As Chapter 28’s discussion of corporate portfolio management indicates, any program to create value should include systematically reviewing your portfolio of businesses. In our analyses of the largest global exchange-listed companies, those that endure at the top ranks combine their mergers and acquisitions (M&A) programs with selected divestitures, including shedding businesses performing well that could do better under different ownership. Evidence shows that divestitures lead to higher shareholder returns in the short term around their announcement, as well as in the years following the divestiture, especially for companies employing such a balanced portfolio ...

Get Valuation, 7th Edition now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.