July 2011

Beginner

288 pages

7h 22m

English

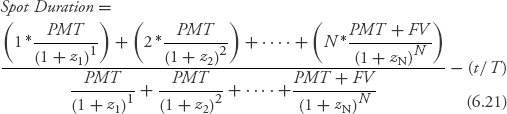

A number of versions of duration have been introduced since Macaulay first wrote down a formula for the statistic in the 1930s. I always wonder: Does this mean he invented it or discovered it? Anyway, another version that I'll call spot duration sometimes is used in academic fixed-income research.

This looks much like the weighted-average formula for Macaulay duration in equation 6.14. The difference is that instead of discounting the cash flows with the yield to maturity, the sequence of spot, or zero-coupon, rates (z1, z2, … , zN) is used. The price of the bond in the denominator is the same as in equation 6.14

Read now

Unlock full access