19

Long Straddles

What is a long straddle? A long straddle consists of two legs, a long call and a long put with the same strike and from the same series. Buying a straddle involves buying both options simultaneously.

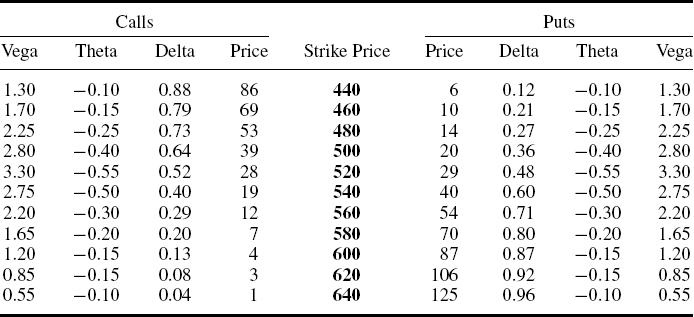

For example, from the matrix of Sep BP option prices (Table 19.1, repeated from Table 16.1), buying the 520 straddle consists of two legs, buying the 520 call at 28 and simultaneously buying the 520 put at 29. The cost of the straddle is 57 ticks (equivalent to £570) per straddle, the sum of the 28 paid for the 520 call and the 29 paid for the 520 put. These 57 ticks represent the maximum loss on buying the straddle. This loss will occur if BP is at exactly 520 (i.e. £5.20) on Sep expiry, since both the 520 calls and 520 puts will expire worthless. The maximum possible value of the straddle is unlimited to the upside and limited only by zero to the downside.

Table 19.1 LIFFE Sep BP option prices and Greeks at close on 21 July 2008 (BP share price (LSE) = 522 (i.e. £5.22))

The risk/reward for buying the 520 straddle at 57 is a potential loss of 57 ticks (equivalent to £570) per straddle against unlimited potential profit, favourable “odds” of infinity to 1. Why would we buy this straddle?

Remember the two key factors when deciding upon option strategy are our view on the underlying and our view on volatility (are the options cheap or expensive?). If we are buying a ...

Get Equity and Index Options Explained now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.