June 2008

Beginner to intermediate

440 pages

11h 56m

English

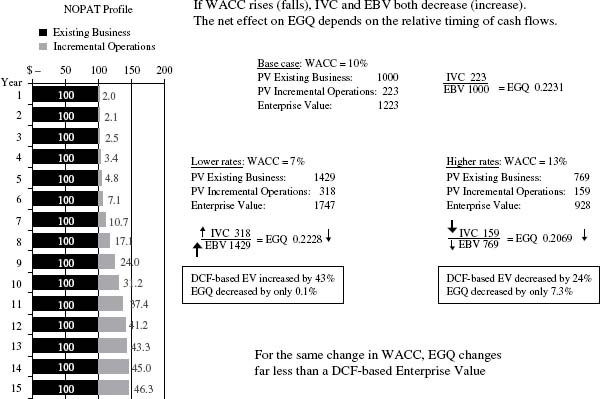

Provided the initial cost of capital assumption is a reasonable estimate (we base it on CAPM), EGQ will very reliably measure a company's value-added growth potential relative to its EBV without distortions caused by an incorrect cost of capital assumption. This allows investors to compare the worth of a company's expected value-added growth potential (relative to the value of its existing earnings) to that of peer companies without distortions from minor inaccuracies in the assumed cost of capital. This allows EGQ regressions to identify the market's assigned cost of capital for a group of peer companies independent of the cost of capital assumptions made in the DCF to calculate company EGQs.

Consider a firm with yearly NOPAT from existing business of $100 and incremental opportunities as shown in Figure 28.1.

Figure 28.1 EGQ is less sensitive to changes in WACC than most valuation models

Figure 28.1 demonstrates important aspects of EGQ related to the assumed cost of capital.

Read now

Unlock full access