A GENERAL DESCRIPTION OF THE STATEMENT OF CASH FLOWS

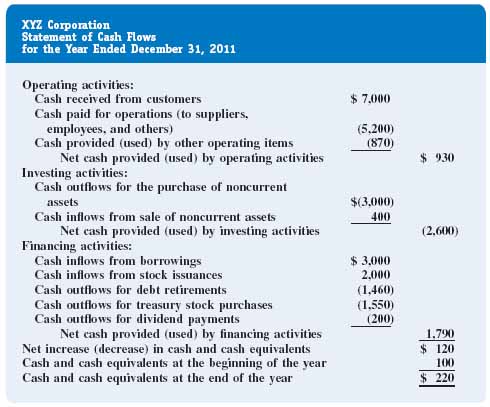

Take a moment now and refer back to Chapter 2. It describes the statement of cash flows in terms of the other financial statements, explaining the change in the cash balance from one balance sheet date to the next. Figure 14-2 illustrates the statement of cash flows more completely. This statement is divided into three sections (operating activities, investing activities, and financing activities) and shows the cash inflow and outflow categories that normally comprise each section.

1. Commercial paper and short-term debt instruments were discussed in Chapter 10. Also, some corporations, like McDonnell Douglas, Eli Lilly, and Walt Disney, also include short-term investments, such as marketable securities, in the definition of cash for purposes of the statement of cash flows. Such a practice is acceptable under generally accepted accounting principles because marketable securities, by definition, are highly liquid.

FIGURE 14-2 Standard statement of cash flows

Cash Provided (Used) by Operating Activities

Cash provided (used) by operating activities includes those cash inflows and outflows associated directly with the acquisition and sale of the company's inventories and services. This category includes the cash receipts from sales and accounts receivable as well as cash payments for the purchase of inventories, payments on accounts ...

Get Financial Accounting: In an Economic Context now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.