September 2022

Beginner

560 pages

17h 36m

English

This section proves that i) the regression hedge minimizes the variance of the P&L of the hedged portfolio; and ii) the volatility of the regression‐hedged portfolio equals the DV01 of the position being hedged times the standard deviation of the regression residuals.

Begin with least‐squares estimation, which finds the parameters ![]() and

and ![]() to minimize,

to minimize,

To solve this minimization, differentiate (A6.1) with respect to each of the parameters, set each result to zero, and obtain the following two equations,

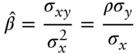

These equations can be solved to show that,

where and are the sample averages; and the standard deviations; the covariance; and the correlation. ...

Read now

Unlock full access