Chapter 14

MANAGERIAL ACCOUNTING

CHAPTER LEARNING OBJECTIVES

After studying this chapter, you should be able to:

- Explain the distinguishing features of managerial accounting.

- Identify the three broad functions of management.

- Define the three classes of manufacturing costs.

- Distinguish between product and period costs.

- Explain the difference between a merchandising and a manufacturing income statement.

- Indicate how cost of goods manufactured is determined.

- Explain the difference between a merchandising and a manufacturing balance sheet.

- Identify trends in managerial accounting.

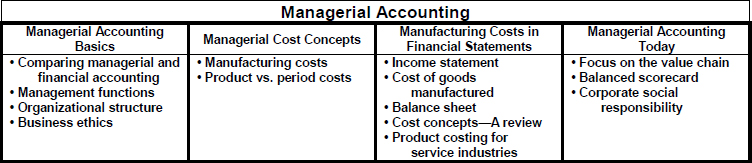

PREVIEW OF CHAPTER 14

Beginning with this chapter, we turn our attention to issues such as the costs of material, labor, and overhead and the relationship between costs and profits. In a previous financial accounting course, you should have studied the form and content of financial statements for external users such as stockholders and creditors. These statements represent the principal product of financial accounting. The chapters in this textbook focus primarily on the preparation of reports for internal users, such as the managers and officers of a company. These reports are the principal product of managerial accounting. The content and organization of this chapter are as follows:

CHAPTER REVIEW

Managerial Accounting Basics

- (L.O. 1) Managerial accounting provides economic and financial information for ...

Get Study Guide Vol 2 t/a Accounting: Tools for Business Decision Makers, 5th Edition now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.