Chapter 21

BUDGETARY PLANNING

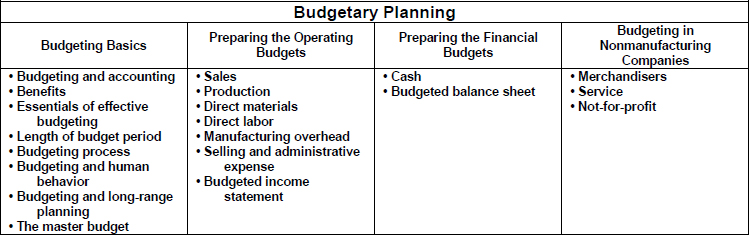

CHAPTER LEARNING OBJECTIVES

After studying this chapter, you should be able to:

- Indicate the benefits of budgeting.

- State the essentials of effective budgeting.

- Identify the budgets that comprise the master budget.

- Describe the sources for preparing the budgeted income statement.

- Explain the principal sections of a cash budget.

- Indicate the applicability of budgeting in nonmanufacturing companies.

PREVIEW OF CHAPTER 21

Our primary focus in this chapter is budgeting—specifically, how budgeting is used as a planning tool by management. Through budgeting, it should be possible for management to maintain enough cash to pay creditors, to have sufficient raw materials to meet production requirements, and to have adequate finished goods to meet expected sales. The content and organization of this chapter are as follows:

CHAPTER REVIEW

Budgeting Basics

- (L.O. 1) A budget is a formal written statement of management's plans for a specified time period, expressed in financial terms.

- The role of accounting during the budgeting process is to (a) provide historical data on revenues, costs, and expenses, (b) express management's plans in financial terms, and (c) prepare periodic budget reports.

Benefits of Budgeting

3. The primary benefits of budgeting are as follows:

a. It requires all levels of management to plan ahead.

b. It provides definite objectives for ...

Get Study Guide Vol 2 t/a Accounting: Tools for Business Decision Makers, 5th Edition now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.