May 2018

Intermediate to advanced

434 pages

21h 6m

English

where ![]() may contain the intercept and a polynomial time trend. KPSS test is then an Lagrange multiplier (LM) test:

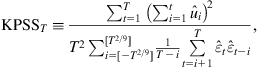

may contain the intercept and a polynomial time trend. KPSS test is then an Lagrange multiplier (LM) test:

(4.33)

(4.33)

(4.33)

where the denominator is an estimator of the residual spectrum at frequency 0, in this case written already to reflect a Newey–West automatic, data-driven bandwidth choice as in Example 4.3.10 Example 4.4 shows the PP and KPSS tests at work.

Read now

Unlock full access