April 2008

Intermediate

832 pages

26h 2m

English

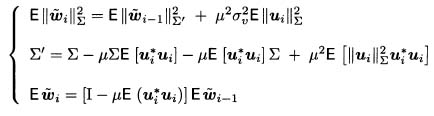

We use the mean and variance relations of the last chapter to study the transient perfor mance of the LMS algorithm,

for which the data normalization in (22.2) is given by

In this case, relations (22.26)–(22.27) and (22.29) become

We therefore need to evaluate the three moments:

The first two moments are obvious, and can be evaluated regardless of any assumed distribution for the regression data since

The difficulty lies in evaluating the last moment in (23.4). To do so, we shall treat two cases. First we treat the case of Gaussian regressors for which the last moment can be evaluated explicitly. Afterwards, we treat the general case of non-Gaussian regressors.

We assume in this chapter that the regressors {ui} arise from a circular Gaussian distribution with covariance ...

Read now

Unlock full access