Chapter 21

Portfolio Construction Principles

The Problem with Portfolio Optimization

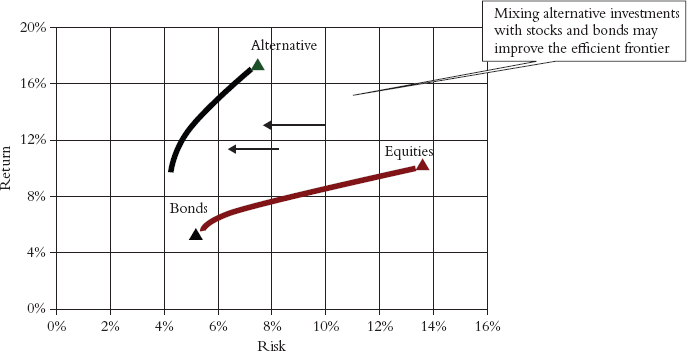

Portfolio construction would seem to be a simple task given the availability of portfolio optimization software, which requires the input of only the returns for the holdings in the portfolio and provides the optimal allocations based on this input. The software will provide an efficient frontier curve, which consists of the portfolios (that is, allocation mixes) that result in the highest return for any target level of volatility. (Two efficient frontier curves—one including only stocks and bonds and the other adding alternatives to the mix—are illustrated in Figure 21.1.) If the investor decides an 8 percent annualized volatility is the desired target risk level for the portfolio, the portfolio corresponding to an 8 percent volatility on the efficient frontier curve will be the mix of assets that provides the highest return for an 8 percent volatility. So it would seem that all the investor has to do is choose the list of investments and the desired portfolio volatility level and, presto, the software would provide the mathematically derived optimal percentage allocation for each holding. Not much decision making or heavy lifting required here.

Although portfolio optimization provides an easy and ...

Get Market Sense and Nonsense: How the Markets Really Work (and How They Don't) now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.