May 2012

Intermediate to advanced

846 pages

27h 56m

English

2.19 EXEMPTIONS FROM OTHER IFRSS

2.19.1 Share-Based Payment Transactions

2.19.1.1 Exemption Explained

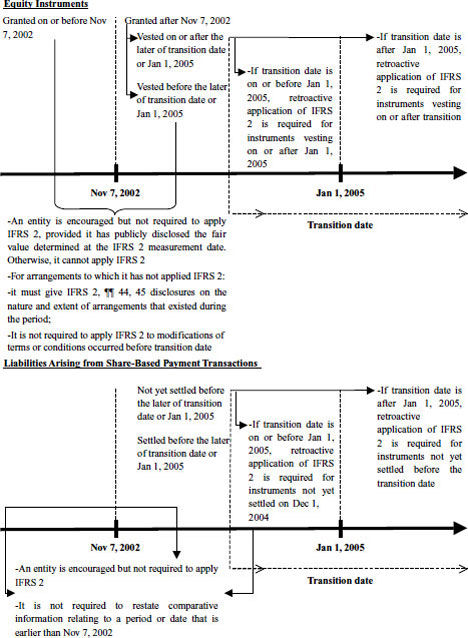

IFRS 1 permits some relief from IFRS 2 based on date of grant and date of vesting of share-based instruments.582 Exhibit 2-23 illustrates this exemption.

Exhibit 2-23 Share-Based Payment Transaction Exemption under IFRS 1

A European survey indicates that all 2005 first-time adopters used this exemption, when available.584 A 2005 survey of 45 IFRS first-time adopters illustrates that approximately 58% used this exemption.585 A survey of interim reports of 144 listed companies in FTSE 101-350 in 2005 converting from UK GAAP to IFRSs reveals that 76% availed themselves of this exemption.586

2.19.1.2 Implications for Accounting Estimates

Paragraph 2.11.14 previously explains the implications on ...

Read now

Unlock full access