146 Numerical Methods and Optimization: An Introduction

t

y(t

1

)

y

1

y

0

t

0

t

1

y = y(t)

y

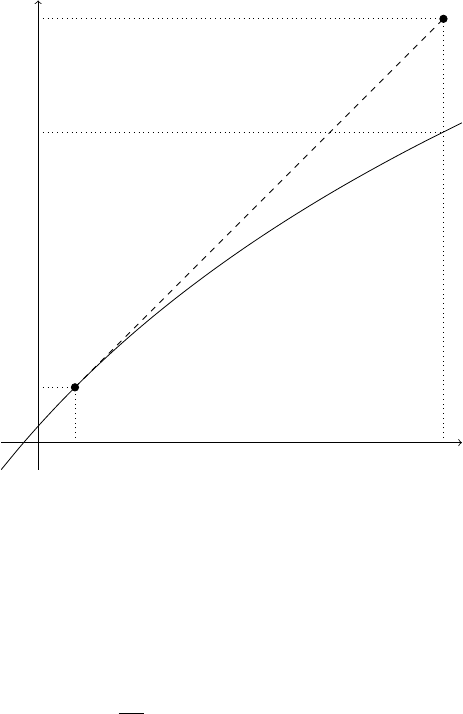

FIGURE 7.1: An illustration of the one-step Euler method.

Example 7.6 Suppose that we have a 30-year 10% coupon bond with yield to

maturity λ

0

= 10% and price P

0

= 100. We are interested to know the price of

this bond when its yield changes to λ

1

= 11%. We can use the price sensitivity

formula mentioned in Example 7.1:

dP

dλ

= −PD

M

, with P (λ

0

)=P

0

.

Let us use Euler’s method to solve the above equation. We have

f(λ, P )=−PD

M

; λ

0

= 10; P

0

= 100; h =0.11 − 0.10 = 0.01;

f(λ

0

,P

0

)=−P

0

D

M

(0.10, 2, 30, 0.10) = −100 · 9.47 = −947.

Therefore,

P (λ

1

) ≈ 100 + 0.01(−947) = 100 − 9.47 = 90.53.

Example ...